The Indian gold loan industry entered FY26 already in motion: a regulator that had demonstrated its willingness to shut down large lenders, a gold price cycle that was steadily expanding collateral values, and a competitive dynamic between banks and specialist NBFCs that had been shifting for structural reasons.

Over the twelve months that followed, three forces shaped the sector:

- Regulatory consolidation — the RBI moved from episodic enforcement toward a harmonised, unified framework.

- Gold price appreciation — rising collateral values expanded borrowing capacity across all portfolios.

- Balance-sheet competition — banks accelerated their push into gold lending while specialist NBFCs scaled operations.

By December 2025, the organised gold loan market had already crossed ₹15 trillion — a milestone projected for 2027 as recently as 2024 — while regulatory expectations for the sector were clearer than at any point in the previous decade.

OPENING POSITION: APRIL 1, 2025

The year began with the industry still absorbing the consequences of two major regulatory actions from 2024.

In March 2024, the RBI imposed a temporary ban on fresh gold loan disbursements by IIFL Finance after identifying serious irregularities in lending practices — including gold valuation without borrower presence, LTV breaches, and non-standard auction processes. The restriction was lifted in September 2024, but it triggered sector-wide inspections and fundamentally altered the compliance posture of every NBFC in India.

Separately, Asirvad Microfinance, a subsidiary of Manappuram Finance, faced restrictions on fresh lending in October 2024 alongside several other MFIs, on grounds of excessive interest spreads. Those restrictions were lifted on January 8, 2025.

Both events signalled a regulatory environment that had become far less tolerant of operational lapses in secured retail lending.

Gold opened the year at ₹92,840 per 10 grams (24K retail, April 1, 2025). The organised market — banks and NBFCs combined — stood at ₹11.8 trillion as of March 2025, per ICRA. PSU banks were aggressively leveraging their lower cost of funds to challenge NBFCs on their traditional turf.

ACT I: THE REGULATORY YEAR

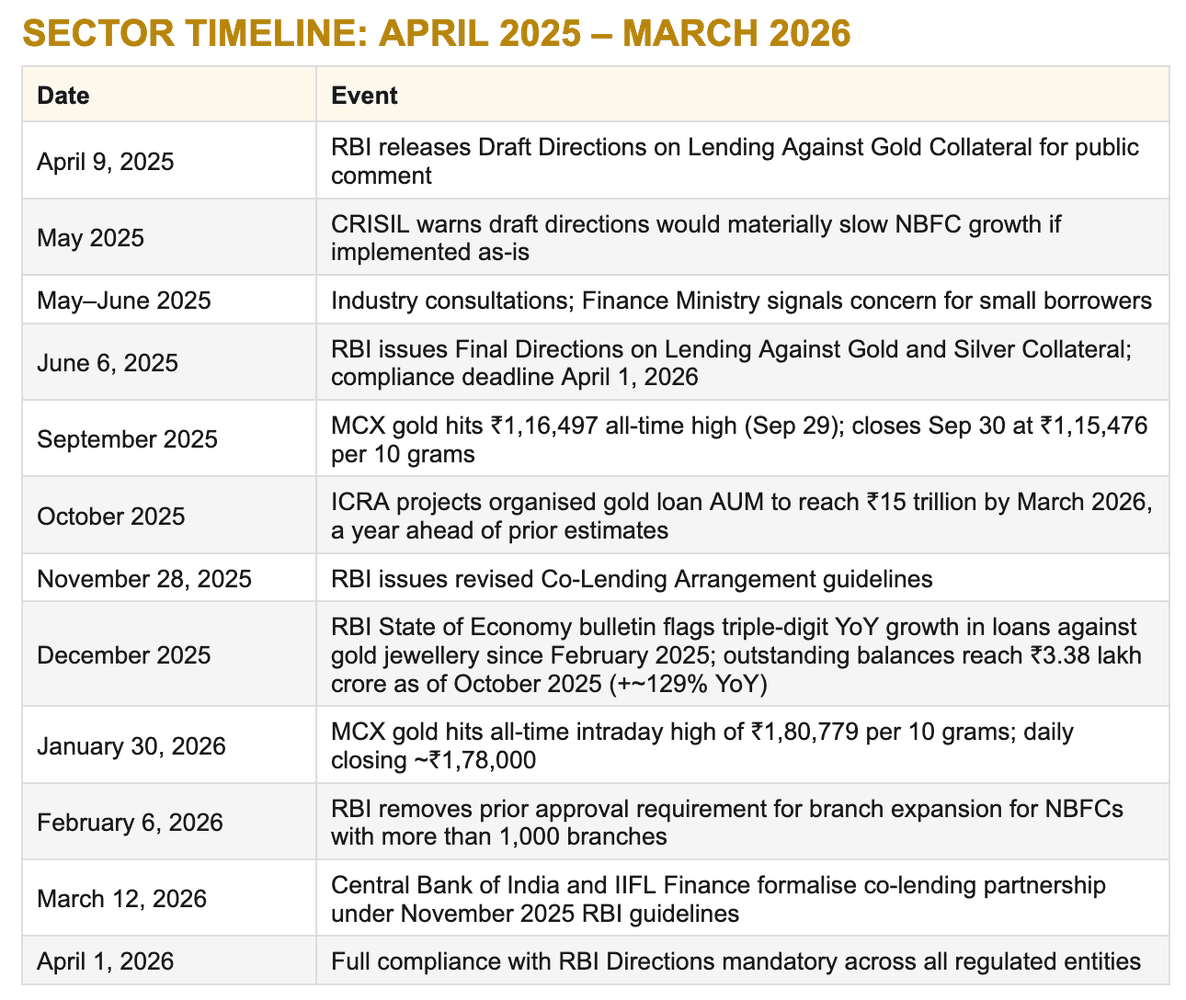

The Draft and the Pushback (April – May 2025) On April 9, 2025, the RBI published Draft Directions for public comment — the most significant proposed intervention in gold lending in a decade. The draft proposed tiered LTV ratios, mandatory borrower presence during valuation, hard limits on bullet loan tenures, formal credit assessment for loans above ₹2.5 lakh, and a prohibition on using loan proceeds to purchase gold.

CRISIL Ratings responded in May with a clear warning: if implemented as-is, the directions would materially slow gold loan NBFC growth, with the bullet loan cap and credit assessment requirement falling disproportionately on specialist lenders relative to banks.

During this consultation period, the Finance Ministry also signalled that regulatory tightening should avoid unintended consequences for small borrowers, many of whom rely on gold loans for emergency liquidity. The industry’s concern was heard: the final directions removed the proposed distinction between banks and NBFCs for income-generating loans, creating uniform treatment across entity types. The final product was a negotiated outcome, not a diktat.

A Note on Valuation Governance One underappreciated aspect of the framework was the RBI’s focus on valuation governance. Historically, fraud in the gold loan sector has originated not from borrower default but from valuation manipulation — appraisers certifying incorrect purity, disbursals made at peak intraday prices, gold valued without the borrower present. The new framework addresses each of these directly, representing a structural improvement in risk management across the industry.

The Harmonized Framework (June 6, 2025) The final RBI Directions, issued June 6, 2025, established a unified framework across all regulated entities — commercial banks, NBFCs, co-operative banks, and housing finance companies. Compliance deadline: April 1, 2026.

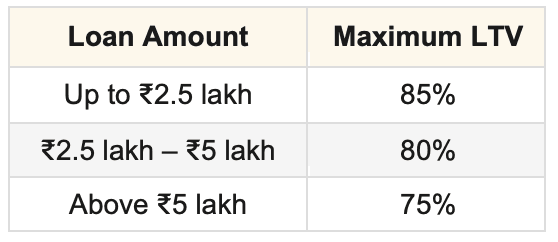

The LTV Restructure. The previous flat 75% cap was replaced with a tiered structure keyed to loan size. The LTV must be maintained on an ongoing basis throughout the loan tenor, not just at disbursement:

The Prudence Formula. Gold valuation now uses the lower of the 30-day average closing price or the previous day’s closing price, published by IBJA or a SEBI-recognized exchange. This ended the practice of disbursing against peak intraday prices to maximise loan size.

The Silver Pivot. In a first, the RBI formally allowed silver ornaments and coins (minimum 92.5% purity) as eligible collateral, opening a high-yield niche for rural lenders.

The End-Use Prohibition. Loan proceeds cannot be used to purchase gold in any form — jewellery, coins, ETFs, or mutual funds. The RBI had identified speculative recycling — borrow against gold, use proceeds to accumulate more gold, repeat — as a systemic concern. This provision closes it.

The Bullet Loan Cap. Principal and interest must be cleared within 12 months. Renewals are permitted only for standard-classified accounts after accrued interest is cleared.

The Expansion Reward (February 6, 2026) In a significant nod to the sector’s stabilisation, the RBI scrapped the prior approval requirement for branch expansion for NBFCs operating more than 1,000 branches. Muthoot Finance (~6,000 branches) and Manappuram Finance (~5,000 branches) can now scale without individual regulatory friction. This was interpreted widely as a signal that the regulator believed the sector had stabilised after the enforcement actions of 2024.

ACT II: GOLD — THE COLLATERAL ENGINE

Gold price movements in FY26 were the rising tide that lifted AUMs, ticket sizes, and profits across the board.

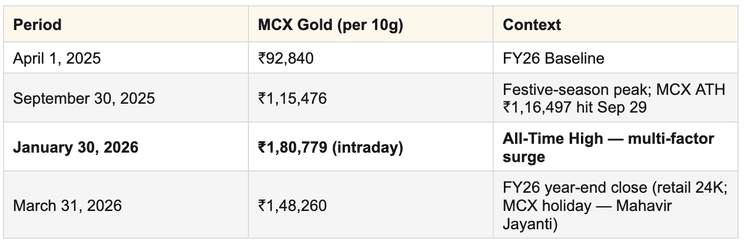

The year’s intraday peak — ₹1,80,779 per 10 grams — was hit on January 30, 2026, driven by global demand, a softer rupee, and sustained ETF inflows. Daily closing was around ₹1,78,000. Gold then corrected sharply: by March 24 it had touched a low near ₹1,36,000–1,40,000 (a ~25% intraday pullback from the ATH), before partially recovering on Israel-Iran conflict escalation fears. FY26 closed on March 31 at ₹1,48,260 per 10 grams (retail 24K; MCX was shut for Mahavir Jayanti), ~18% below the January intraday peak.

The price vs. tonnage reality. The massive AUM growth this year was price-led, not tonnage-led. Physical gold tonnage held by NBFCs grew at only ~1.7% CAGR from FY2020 to FY2025, while AUM grew at ~20% over the same period. Collateral revaluation, not new customer acquisition, did the heavy lifting.

The systemic risk. Rising prices have self-cured marginal LTV breaches throughout the year — borrowers in stress could refinance because their collateral kept appreciating. A sustained sharp correction could eliminate those buffers overnight, potentially triggering mandatory auctions at scale.

ACT III: THE LENDER DIVIDE

Muthoot Finance: The Year It Pulled Away Muthoot’s FY26 was the strongest in its 85-year history. It’s pure-play gold loan model meant every rupee of price appreciation flowed almost entirely to AUM and margin. Average AUM per branch reached ₹25.15 crore by H1 FY26, up from ₹21.21 crore at the start of the year. 9M FY26 Standalone PAT: ₹7,048 crore, up 91% YoY.

Q3 FY26 Standalone PAT: ₹2,656 crore, up 94.88% YoY.

Consolidated Loan AUM (December 31, 2025): ₹1,64,720 crore, up 48% YoY.

The February 2026 branch expansion relaxation landed as a further growth catalyst, allowing Muthoot to scale its ~6,000-branch network without regulatory lag.

Manappuram Finance: The Multi-Front War Gold AUM grew to ₹38,754 crore in Q3 FY26, up 58.2% YoY. Consolidated profits were dragged down by impairment charges in microfinance (Asirvad, which spent Q2 FY25 under an RBI disbursement ban for excessive interest spreads) and vehicle finance. The gold book is booming. It is currently subsidising the recovery of the MFI subsidiary.

IIFL Finance: The Co-Lending Comeback Exactly 12 months after its gold loan ban was lifted, IIFL’s gold loan AUM grew 2.2x from its post-ban low (S&P, citing data to September 30, 2025), reaching a gold loan AUM of ₹43,432 crore as of December 31, 2025, across 4,761 branches.

On March 12, 2026, IIFL formalised a co-lending partnership with Central Bank of India under the RBI’s revised Co-Lending guidelines of November 28, 2025. Under the arrangement, IIFL originates and services loans while the bank co-holds them on its balance sheet — giving IIFL access to a lower blended cost of funds without fully consuming its own balance sheet. S&P revised IIFL’s outlook to “Positive,” specifically citing gold loan market share recovery.

The recovery reinforced a structural feature of the gold loan industry: branch presence and local customer relationships are extremely resilient competitive assets. Customers came back.

ACT IV: THE MARKET

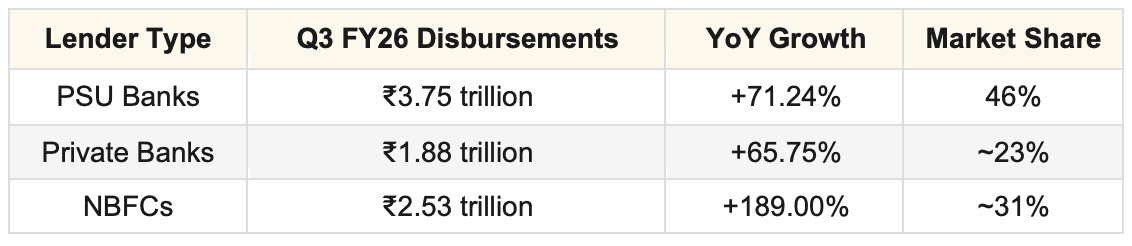

Why Banks Expanded The rapid expansion of bank gold loan portfolios has a regulatory origin. In November 2023, the RBI increased risk weights on unsecured retail lending — personal loans and credit cards. This made unsecured lending more capital-intensive for banks. Gold loans offered an attractive alternative: fully collateralised, low credit risk, quick disbursement. As a result, many banks accelerated gold loan campaigns across their branch networks through FY25 and into FY26.

The NBFC Operational Edge Despite banks’ structural funding advantage, specialist gold loan NBFCs retain a significant operational edge. The business requires rapid valuation, branch-level decision-making, secure collateral handling, and efficient auction mechanisms — capabilities deeply embedded in NBFC operating models but often less developed within large universal banks. This is why NBFCs, despite ceding stock share to banks, continue to grow faster in new loan flow.

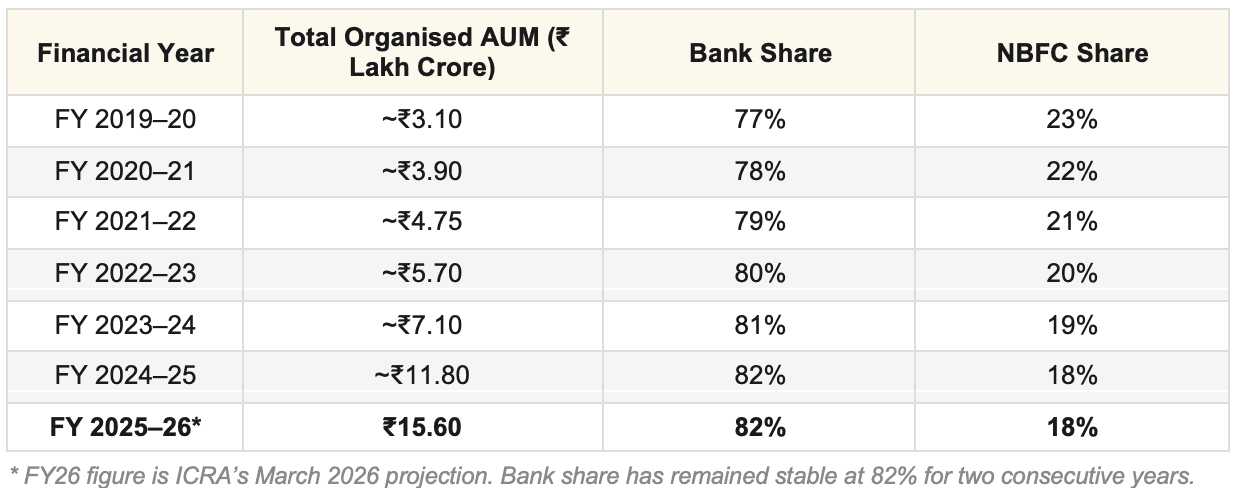

The Shift in Market Share Competitive trajectory (ICRA data):

The Scale of the Boom India’s total gold loan portfolio — spanning retail, business, and priority sector loans across banks and NBFCs — reached ₹16.2 lakh crore as of December 2025 (CRIF High Mark, Q3 FY26 report), up 44.1% YoY. This made gold loans the fastest-growing category in India’s ₹162.7 lakh crore retail lending market, overtaking personal loans in portfolio outstanding for the first time.

A note on the RBI figure that appears in most coverage: the RBI’s December 2025 State of the Economy bulletin cites ₹3.38 lakh crore growing at ~128% YoY as of October 2025. That number covers only ‘loans against gold jewellery’ at scheduled commercial banks — the retail, non-agricultural sub-segment. It excludes priority sector gold loans at banks (~₹4.8 lakh crore) and NBFC gold loans. Both figures are accurate; they are measuring different parts of the same market.

Q3 FY26 originations (CRIF High Mark): Total gold loan originations reached ₹8.18 lakh crore, up 90.3% YoY:

The Urban Shift Historically, gold loans were concentrated in rural and semi-urban India. Increasingly, urban borrowers are using gold loans for small business working capital, short-term liquidity, and bridge financing. The stigma once associated with pledging jewellery has declined significantly as banks and large NBFCs offer the product through mainstream branch networks. Over 60% of new retail loan originations still come from semi-urban and rural regions, but the urban segment is expanding, driven by higher ticket sizes and the normalisation of the product.

The Delinquency Picture The credit quality story in gold loans is more nuanced than headline NPA numbers suggest — and it has changed significantly over FY26. A comparison using CRIF High Mark’s December 2025 data:

Early-stage delinquency (PAR 31–90): NBFC gold loans stood at 2.11% in December 2024, PSU banks at 1.44%, private banks at 1.75%. By December 2025, NBFC PAR 31–90 had dropped sharply to 0.82% — one of the sharpest single-year improvements across any retail credit segment. PSU banks fell to 1.02%, private banks to 1.15%.

Near-NPA delinquency (PAR 91–180): PSU banks stood at 0.07% in December 2025, private banks at 0.14%, NBFCs at 0.25%. The absolute levels across all lenders are low and improving. Gold loans’ PAR 31–180 (combined) declined from 2.4% in December 2024 to 1.8% in December 2025 (CRIF).

The risk is structural, not current. Rising prices have self-healed marginal LTV stress throughout FY26 — borrowers could refinance because their collateral kept appreciating. A sustained correction reverses this: collateral values fall, LTV buffers compress, and the bullet loan rollover model that NBFCs depend on becomes acutely exposed. The FY26 delinquency data looks healthy precisely because prices ran in the industry’s favour all year. The risk is in the next cycle, not the current book.

THE CLOSE: MARCH 31, 2026

The organised gold loan market crossed the ₹15 trillion mark by December 2025 — three months ahead of ICRA’s October 2025 projection, which had itself pulled forward a milestone originally not expected until 2027. CRIF High Mark’s Q3 FY26 report confirms total gold loan portfolio outstanding at ₹16.2 lakh crore as of December 2025, up 44.1% YoY. ICRA’s forward trajectory extends to ₹18 trillion by FY27. ICRA projects NBFC gold loan AUM to grow 30–35% in FY26, with favourable LTV regulations and rising gold prices the primary drivers.

As of today, April 1, 2026, the new RBI Directions are in full effect. The shame premium on gold pledging has vanished, replaced by a strategic urban liquidity tool. A gold loan is ultimately a simple transaction: a household asset converted into liquidity within minutes. As long as Indian households continue to hold vast quantities of gold jewellery, the sector will remain one of the country’s most resilient forms of secured credit.

SOURCES

RBI Draft Directions, April 9, 2025 • RBI Final Directions on Lending Against Gold and Silver Collateral, June 6, 2025 • CRISIL Gold Loan NBFC Reports, May 2025 and January 2026 • ICRA Gold Loan Market Report, October 2025 • Muthoot Finance Investor Presentation Q3 FY26 • Manappuram Finance Investor Presentation Q3 FY26 • Equifax India Gold Loan Disbursement Report Q3 FY26 • RBI State of Economy Bulletin, December 2025 • CRIF Gold Loan NPA Data, March 2025 • MCX Historical Data • Central Bank of India–IIFL Finance Co-Lending Announcement, March 12, 2026