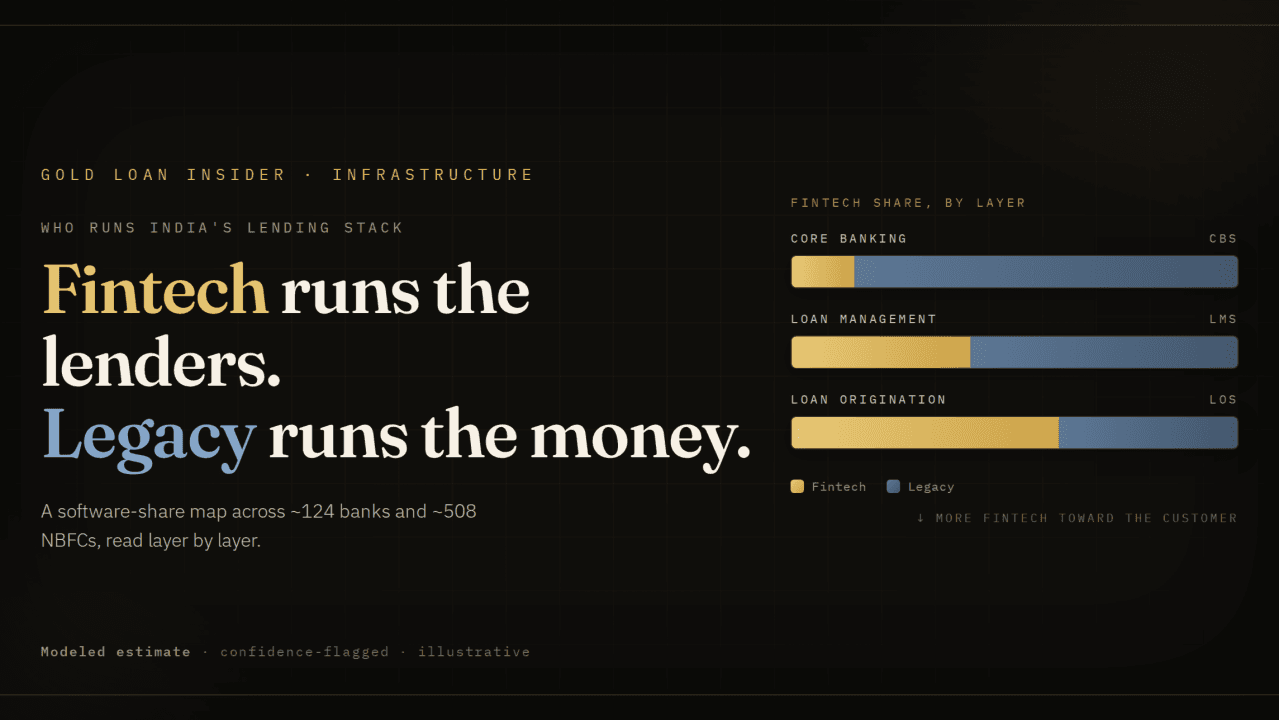

Who runs India's lending stack: fintech vs legacy?

A software-share map across ~124 banks and ~508 large NBFCs. The count and the money point in opposite directions.

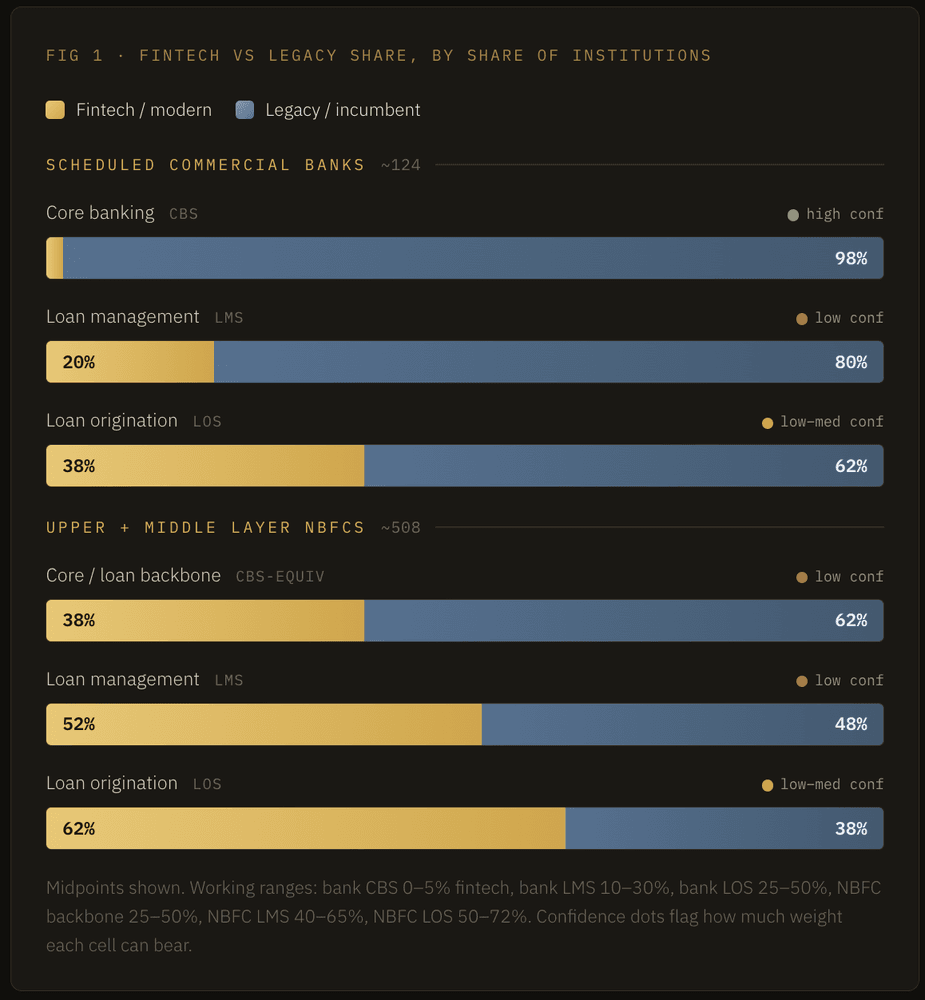

India runs its formal credit on roughly 124 scheduled commercial banks and about 508 NBFCs large enough for the RBI's upper or middle layer. Underneath each one sit broadly three software layers: the core banking system, loan origination, and loan management. How much of that stack is now fintech-built, and how much is still legacy?

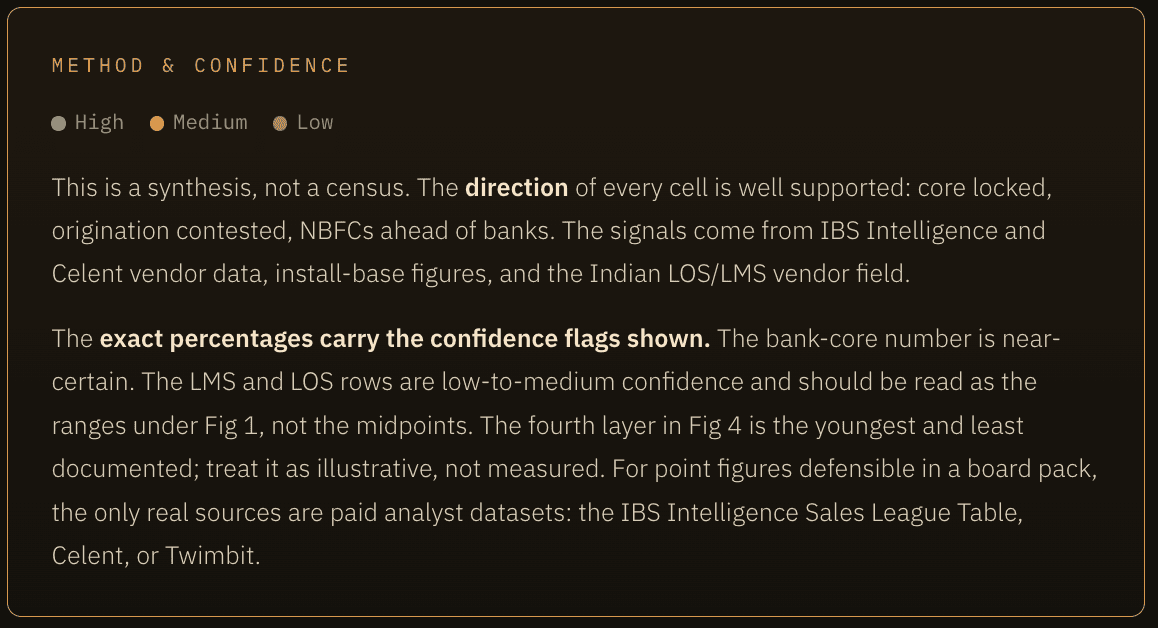

Not sure if there's a published answer. I couldn't find a survey covering all 632 institutions by software layer. So following is a model (not measurement). I have marked a confidence level on every figure and put the method at the end.

What is FinTech :-)

"Legacy organisations often call themselves FinTech & FinTechs wish they were Legacy"

First, the line between fintech and legacy has to be defined.

Legacy is the incumbent set: Finacle, TCS BaNCS, Oracle FLEXCUBE, Nucleus FinnOne, C-Edge, and the in-house cores banks wrote for themselves. Fintech is the cloud-native, API-first generation: Lentra, Finflux (now part of M2P), Finezza, CloudBankin, AllCloud, Perfios, and the global cloud cores such as Zeta and Mambu.

One grey zone is worth naming. Newgen and Nucleus have re-platformed older products onto cloud-native, low-code architecture. Count their new deployments as fintech and the origination figures below rise by about ten points. Count their installed base as legacy and they fall. I have split the difference: old base as legacy, new cloud wins as fintech.

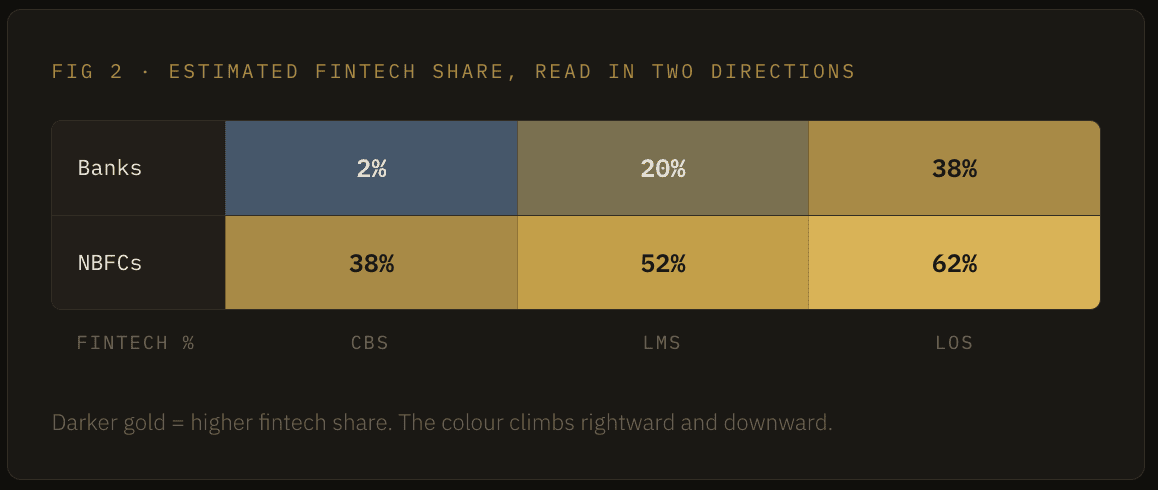

Read by share of institutions, the pattern is clear. Banks are legacy at the core and contested at origination. NBFCs are the mirror image: fintech-led, maybe because most of them never had a legacy core to defend?

The core layer is close to settled. Almost every scheduled bank runs Finacle, BaNCS, or FLEXCUBE as its licensed core. Cloud-native cores appear only inside carve-out digital units, not as the primary system. That is the one cell I hold with high confidence: fintech core share among banks sits in low single digits.

Origination is a battleground. Private banks and a growing set of public-sector banks now run fintech origination engines over their legacy cores, because origination can be swapped without touching the ledger. NBFCs go further. The middle layer is full of mid-size lenders that buy a cloud platform rather than build one, which is why fintech origination share among NBFCs is the highest cell on the board.

Two gradients

The grid moves two ways at once. Left to right, fintech share climbs as you go from core to origination. The closer a layer sits to the ledger, the more legacy holds; the closer it sits to the customer, the more fintech takes. Replacing origination is a project. Replacing a core is a multi-year, high-risk migration, which is precisely why it rarely happens.

Top to bottom, NBFCs out-fintech banks at every layer. No deposit core, lighter legacy, and a long tail of mid-size lenders with no in-house engineering all push in the same direction.

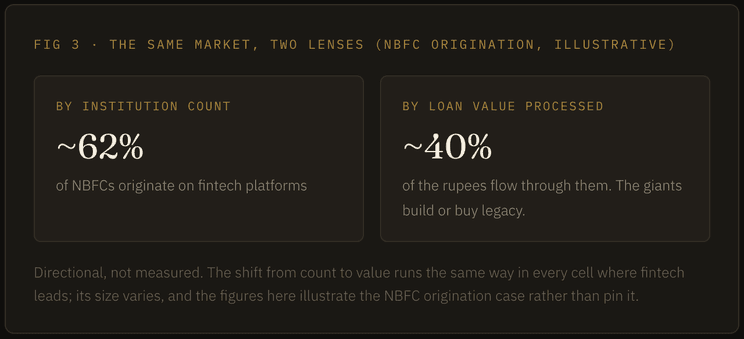

The count is NOT the money

Everything above counts institutions. Switch the lens to loan value, or assets under management, and the picture inverts wherever fintech leads. The institutions that hold most of the book (SBI, the large public-sector banks, Bajaj, Muthoot, the upper-layer NBFCs) all run legacy or custom systems, so a layer that fintech dominates by lender count can shrink to a minority by rupees. The clearest case is NBFC origination: a strong majority of lenders, a much smaller share of the money. The fintech-built lenders are many, but small.

Both statements are true at the same time. Fintech software runs a large share of the lenders. Legacy software still runs most of the money.

"It is the same shape as fintech lending itself: many small players on modern rails, the bulk of the value still on incumbent ones."

The layer the grid does not cover

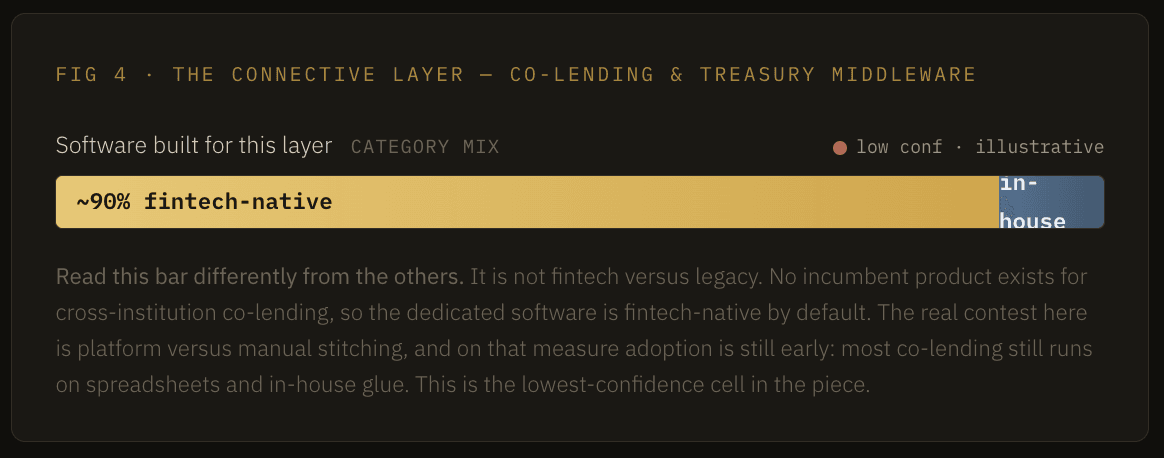

Those three layers sit inside one lender. They say nothing about the layer that connects two. Co-lending, where a bank funds and an NBFC sources, now runs across home, property, gold, vehicle and MSME credit, and it needs software that keeps two institutions' systems in agreement in real time. The legacy core vendors never built for this. There is no Finacle module that splits a single loan between a bank and an NBFC and holds both ledgers, escrow accounts and bureau reports in sync.

So a separate category grew to fill the gap: co-lending and treasury middleware that sits above the core and stitches institutions together. Knight Fintech is among the clearest examples, with its Utopia platform run as secured middleware that integrates with banks and NBFCs without replacing the existing core. Yubi (through its Co.Lend marketplace) and Veefin (from the supply-chain-finance side) work the same seam from different angles.

For any lender whose book leans on co-lending or balance-transfer flows, this is the layer that decides whether a partnership scales or stalls. It is also the youngest, which is why it carries the least data and the most movement.

Summary:

- The core is locked for the planning horizon. If your product depends on replacing a bank's core, the sales cycle runs in years and the incumbents own the relationship. Build alongside the core, not against it.

- Origination is where share actually changes hands. Lowest switching cost, highest fintech momentum. That makes it the place to compete and the place to expect the most crowding.

- The connective layer is the open frontier. Co-lending and treasury middleware has no incumbent to unseat and the most room to run. If partnerships sit at the centre of your model, the platform you choose here matters more than the one running on your core.

Sources & signals: RBI — SCB counts and NBFC layer counts (15 Upper Layer, 493 Middle Layer). IBS Intelligence / Celent 2025–26 — cloud-native wins greenfield and mid-market, incumbents retain tier-one cores. 6sense — vendor install base (India). BlueWeave — India digital banking platform vendors. Decentro, Finezza, Roopya, Newgen, M2P — LOS/LMS vendor landscape. Knight Fintech (3one4 Capital, YourStory), Yubi, Veefin — co-lending and treasury middleware. Figures are the author's modeled estimate built on these signals.