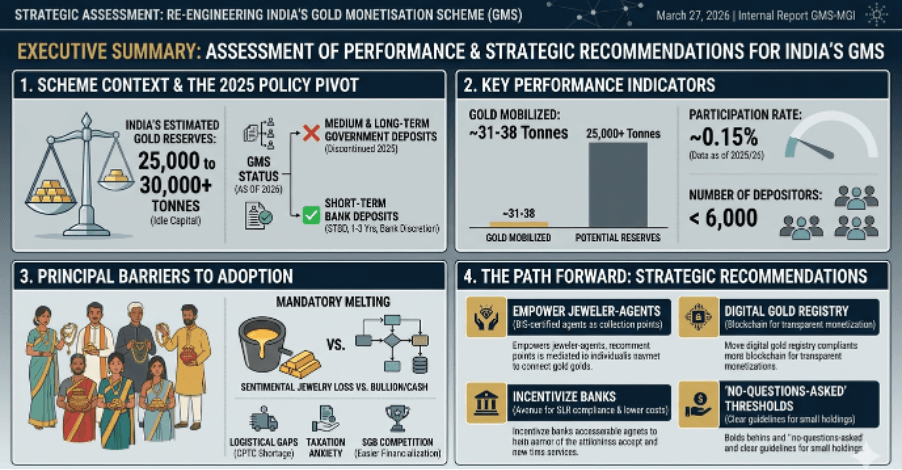

India's households own between 25,000 and 27,871 tonnes of gold. At current prices, that is somewhere north of ₹200 lakh crore sitting in lockers, stitched into the hems of wedding sarees, buried in trust vaults, and stacked in temple sanctuaries. It is, without serious contest, the largest private gold reserve on the planet.

Every few years, a government scheme arrives promising to "mobilise" this gold for the nation's benefit. The Gold Deposit Scheme in 1999. The Gold Monetisation Scheme in 2015. The Sovereign Gold Bond, also 2015. By March 2025, all three had either been wound down or reduced to shadows of their original ambition. The GMS's medium and long-term deposit components were formally discontinued on March 26, 2025. The SGB's last tranche was issued in February 2024 before being quietly shelved.

The cumulative gold mobilised by GMS over a decade: approximately 37.81 tonnes. India imports more than that in two weeks.

The reason these schemes keep failing is not primarily bureaucratic, or even cultural, though both matter. The deeper problem is that India has been trying to solve two fundamentally different problems with one product — and the two problems require mechanisms that directly contradict each other. Until that is acknowledged plainly, every new iteration of the scheme will produce a variation of the same result.

Objective One: Reduce the Import Bill and the Current Account Deficit

India spent $45.54 billion importing gold in FY2024 (April 2023–March 2024), making it the second-largest import item on the national bill after crude petroleum. In FY2024-25, the customs duty on gold was cut sharply from 15% to 6% effective July 24, 2024 — the lowest rate since 2013 — triggering a significant surge in import volumes. According to WGC data, India's domestic gold demand reached 802.8 tonnes in 2024, up from 747.5 tonnes in 2023. Unlike crude, we technically already have this gold. We just cannot access it.

The CAD-reduction logic behind GMS was direct and, in theory, sound. If idle domestic gold is mobilised into the banking system, it can be lent to jewellers as Gold Metal Loans (GML) at commercially competitive rates — typically 7–12% per annum. Jewellers who borrow domestic GML gold have less reason to purchase freshly imported gold. Net import demand falls. The trade deficit narrows.

For this chain to work, the gold must be physically melted and refined to a minimum fineness of 995 parts per thousand. There is no workaround here. A jeweller making a ring needs actual metal to work with. A digital claim on a necklace locked in a vault somewhere is not raw material for manufacturing.

The constraint that cannot be engineered away

Indian household gold is overwhelmingly jewellery, not bars. Jewellery carries form — the specific weight of a particular piece, the design a grandmother wore, the memory of a ceremony. When GMS asks a depositor to surrender that gold for melting, it is not asking for an investment redemption. It is asking for the destruction of an irreplaceable object in exchange for a 1.25% annual yield. No number of policy circulars makes that a compelling transaction.

The Gold Deposit Scheme of 1999, which preceded GMS, set a minimum deposit of 500 grams. In sixteen years, it mobilised a negligible quantity — estimates across sources range from approximately 2 to 15 tonnes — almost entirely from temple trusts with large, anonymous bullion inventories, not households. GMS improved on this by lowering the threshold to 30 grams (later 10 grams), but the emotional barrier remained structurally identical. Smaller threshold, same necklace problem.

What would actually need to change for Objective One to work

The first requirement is genuine last-mile infrastructure. A depositor in a Tier-2 city cannot be expected to travel to a Collection and Purity Testing Centre (CPTC) located hours away, for a net first-year interest income that likely does not cover the petrol. The jeweller-as-agent model — BIS-certified jewellers serving as authorised deposit and assaying points — is the only realistic way to solve this, because jewellers are where households already take their gold. This does not mean jewellers profit from the transaction commercially; it means leveraging an existing trust relationship and physical presence rather than building a parallel network from scratch.

The second requirement is a commercial reason for banks to participate. Currently, banks operating GMS face refining logistics, storage costs, GML risk, and thin margins on a product they did not design. Unless gold held under GMS is allowed to partially satisfy the Statutory Liquidity Ratio (SLR), or banks receive a structured processing fee from the government, the product will remain something banks technically offer and do not meaningfully distribute.

The third requirement is plain communication about existing tax protection. CBDT Instruction No. 1916 establishes that gold holdings up to 500 grams for married women, 250 grams for unmarried women, and 100 grams for men are generally protected from seizure. A significant portion of the population has never heard of this. The "source of wealth" anxiety deterring retail depositors has a specific legal answer — it simply has not been marketed.

The honest assessment of Objective One

Even if all of the above were implemented perfectly, the realistic CAD impact would be modest. India's annual domestic gold demand runs at approximately 750–800 tonnes per year (WGC: 747.5 tonnes in 2023, 802.8 tonnes in 2024). The organised domestic gold recycling infrastructure — refineries, assaying labs, CPTC networks — is not designed for recycling at that scale. Getting GMS to mobilise 50–100 tonnes per year, against annual domestic demand of 750–800 tonnes, is meaningful progress over the current trajectory but not a structural fix to India's gold import dependency. The import is partly driven by fresh manufacturing demand and partly by investment demand; domestic recycling addresses neither driver in full.

GMS is a marginal lever on CAD, not a transformative one. That needs to be said plainly.

Objective Two: Unlock the Financial Value of Household Gold

This is a different problem entirely, and it deserves its own honest treatment.

The question here is not: how do we get India's gold into the manufacturing supply chain? It is: how do households access the economic value of the gold they already own, without selling it or melting it?

The answer already exists at considerable scale. It is called the gold loan market.

According to CRIF High Mark data, India's gold loan portfolio stood at ₹15.6 lakh crore as of November 2025 — a 41.9% year-on-year increase, and nearly double the ₹7.9 lakh crore recorded in November 2023. Gold loans accounted for 9.7% of the entire retail lending portfolio in India, making it the fastest-growing retail credit segment in the country. There were 9.026 crore (902.6 lakh) active gold loan accounts as of November 2025. During the first eight months of FY2025-26, gold loan originations rose 111.1% year-on-year to ₹17.4 lakh crore.

India has already built, largely through market forces rather than government design, one of the world's most extensive gold-backed lending ecosystems. Households walk into a branch — bank or NBFC — pledge their jewellery, receive cash within hours, pay it back, and retrieve their gold intact. The gold is never melted. The emotional relationship with the asset is preserved. The household gets liquidity. The lender earns a spread.

This is Objective Two. It is already working.

Then why does the "no-melt deposit with yield" recommendation keep appearing?

Because the gold loan model and the GMS deposit model are structured in exactly opposite directions. In a gold loan, the household is the borrower — they pay interest to access liquidity against their gold. In a GMS deposit, the household is the lender — they are meant to earn interest for making their gold available to the system.

The appeal of the deposit model is intuitive: instead of paying 9–29% per annum on a gold loan (banks charge ~9–12%; NBFCs, depending on the lender, up to 29%), what if a household could deposit their gold and earn 2–3% per annum while retaining a future claim on the underlying asset? That sounds like a better deal. But it raises a question that dismantles the economics: if the gold is vaulted and not melted, who is paying the depositor's yield, and from what activity?

In the melt model, the answer is clean: the jeweller pays GML interest, which flows through the bank's spread to the depositor. In the no-melt model, the gold is immobilised. There is no GML. There is no manufacturing use. There is no earnings stream.

Three funding mechanisms exist for the yield, and all three break down under scrutiny.

The first is government subsidy — the state pays the yield directly, as the Sovereign Gold Bond did. SGB offered 2.5% annual interest with no offset from any productive deployment of the gold it represented. When gold prices rose from approximately ₹26,300 per 10 grams in 2015 to approximately ₹84,450 by early 2025, the government's total SGB liability grew to ₹1.12 lakh crore. The scheme was discontinued. Any no-melt model with a sovereign yield guarantee carries this exact fiscal risk encoded in its structure. The liability scales with gold prices, and gold prices structurally trend upward.

The second is using the vaulted gold as collateral for cash lending to a third party. The institution issues cash loans against the depositor's gold; the loan interest funds the depositor's yield. But this creates a problem the depositor may not understand: their gold is the collateral for someone else's debt. If the borrower defaults, the depositor's gold is at risk. The depositor has inadvertently become a credit risk provider. This is not a deposit product — it is effectively a secured bond where the household is the unintentional creditor, and it requires regulatory treatment and disclosure that GMS was never designed to provide.

The third option is zero yield — the no-melt model becomes a custody and formalisation product only. The household gets their gold hallmarked, vaulted, insured, and digitally registered. They earn nothing. But they gain verified ownership, loss protection, and potentially faster and cheaper access to gold loans later since the gold is pre-assayed and custodied. This is honest, achievable, and genuinely useful — but it must be sold for what it is, not framed as a yield instrument it cannot deliver.

The real gap in Objective Two

If India's gold loan market is already ₹15.6 lakh crore and growing at 42% year-on-year, the problem is clearly not that a mechanism to unlock financial value from household gold does not exist. It does. The problem is unequal access to it.

Public sector banks hold 59.9% of the gold loan portfolio by value but only 46.6% of active accounts — meaning their average ticket size is large, suggesting they predominantly serve urban, salaried, organised-sector borrowers. Gold loan-focused NBFCs hold only 8.1% of portfolio outstanding but 16.6% of active accounts — smaller tickets, more borrowers per rupee of portfolio, meaning they are already reaching deeper into semi-urban and rural markets.

The underserved population does not need a new deposit scheme. It needs formal gold loan access. The Tier-3 household currently pledging jewellery with an informal moneylender at 36–48% per annum — because the nearest formal branch is two hours away — is not waiting for a government deposit scheme. They are waiting for a formal lender to show up where they live.

The fix is geographic infrastructure and formal credit reach, not a new product category.

The Contradiction Neither Scheme Has Faced Honestly

GMS tried to be both things — a CAD reducer and a financial value unlocker — simultaneously. It could not succeed at either because the mechanisms they require pull in opposite directions.

To reduce CAD, gold must be melted. Melting destroys the sentimental value that makes household gold difficult to mobilise. Resolving that tension requires better infrastructure and incentives, not a redesign of the melt requirement itself.

To unlock financial value without melting, you need a lending mechanism. That lending mechanism already exists as the gold loan market at ₹15.6 lakh crore and growing. The gap is reach, not design.

A scheme that accepts this — that these are two distinct problems requiring two distinct instruments — would look very different from every version of GMS to date.

Instrument One: A genuinely functional melt-based mobilisation scheme, with jeweller-agents, SLR incentives for banks, a marketed CBDT safe harbour threshold, and an honest public acknowledgment that it is a modest but real lever on the import bill.

Instrument Two: An infrastructure push to extend formal gold loan access to underserved geographies — more NBFC branches, lower documentation friction, digital hallmarking that reduces assaying costs — built on the market that already works rather than a sovereign scheme that doesn't.

The discontinuation of GMS's long-term deposits and the SGB in the same twelve-month window is the government acknowledging, in policy language, that the current toolkit is broken. What comes next will depend on whether the redesign starts by asking a simpler question than it has asked before: which of these two problems are we actually trying to solve?

All gold loan market data sourced exclusively from CRIF High Mark: "How India Lends" Reports (FY2023, FY2024, June 2025) and Gold Loan Tracker Report (November 2025). GMS performance data from Ministry of Finance PIB Press Release 2115009 (March 26, 2025) and RBI Master Direction DBR.IBD.No.45/23.67.003/2015-16. Tax protection thresholds from CBDT Instruction No. 1916 (dated May 11, 1994). Import value data from DGCI&S / Ministry of Commerce. Gold demand volume data from World Gold Council India Market Reports (2023, 2024). GML rate range from RBI GMS Master Direction and Bajaj Finserv GML scheme documentation.