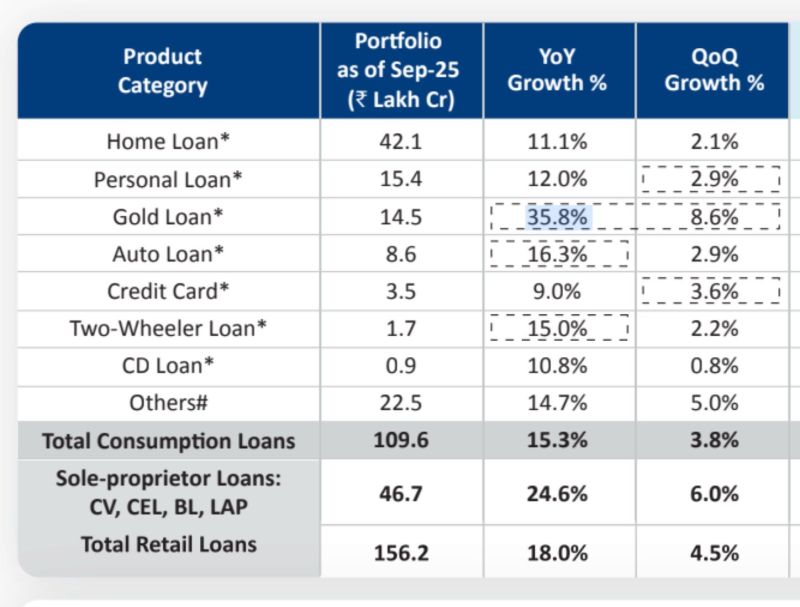

CRIF’s How India Lends (Q2 FY26) suggests gold loans are increasingly a product of choice for India’s self-employed and MSMEs.

𝗞𝗲𝘆 𝘀𝗶𝗴𝗻𝗮𝗹𝘀: 📈 Bigger tickets: Loans >₹5 lakh are now the largest segment by value (30.3%). The ₹2.5–5L band has also expanded meaningfully over the last two years. This is consistent with planned, productive borrowing—not just emergencies.

👤 Self-employed relevance: Short-cycle liquidity and flexible repayments map well to MSME cash flows (inventory, payroll, seasonal working capital).

🆕 New-to-credit entry point: Gold loans have 15% NTC share—a practical gateway to formal credit where bureau histories are thin.

🏘️ Beyond metros: ~32% of originations come from beyond top-100 cities—true mass-market penetration.

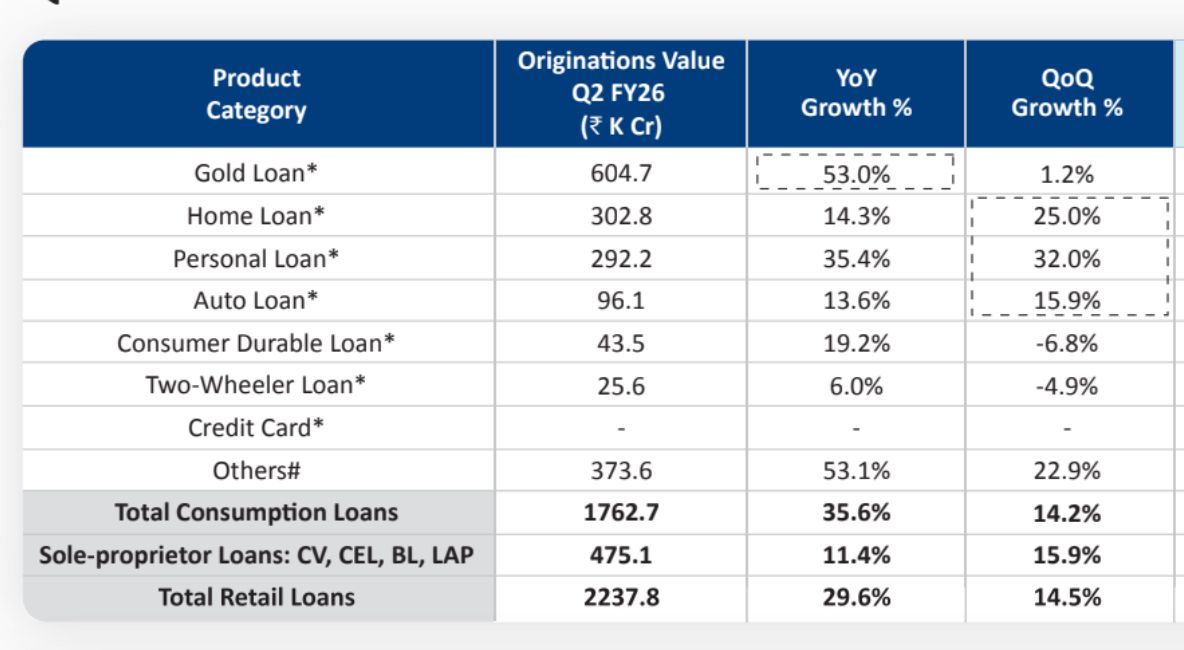

🔄 Secured shift: Gold-loan originations grew 53% YoY, vs 12% for personal loans—reflecting both lender preference and borrower choice for collateral-backed credit.

Why this matters: Indian households hold enormous gold wealth, and a small portion is monetised. Unlocking it responsibly can create affordable, on-tap working capital for the country’s entrepreneurial backbone.

𝗔𝘁 𝗶𝗻𝗱𝗶𝗮𝗴𝗼𝗹𝗱, 𝘄𝗲’𝘃𝗲 𝗯𝗲𝗲𝗻 𝗯𝘂𝗶𝗹𝗱𝗶𝗻𝗴 𝗳𝗼𝗿 𝘁𝗵𝗲 𝘀𝗲𝗹𝗳-𝗲𝗺𝗽𝗹𝗼𝘆𝗲𝗱 𝘀𝗶𝗻𝗰𝗲 𝟮𝟬𝟮𝟬:

✅ Higher cash access via technology-led valuation + LTV discipline

✅ Digital-first servicing (top-ups, renewals, part-release, payments)

✅ Asset-light operating model for better efficiency and experience

✅ Strong risk controls while scaling

Gold loans aren’t just growing—they’re becoming one of India’s most accessible sources of productive capital. We’re excited about what comes next.