The Gold Loan Market Is Growing. The Gold Isn't Moving.

Gold loan companies in India (including indiagold) are trying their best to innovate gold loans. Faster disbursals. Higher LTVs. Doorstep service. Digital apps. The organised gold loan book has crossed ₹15 lakh crore, growing at 30%+ annually. CRIF High Mark put it at 34.6% year-on-year growth in Q1FY26 — the fastest of any consumer credit category in India.

None of it has moved the real number!

Indian households hold approximately 25,000 tonnes of gold — ₹350 lakh crore in household wealth sitting in almirahs, cloth bags, and home safes. The largest private gold stock on earth. A March 2025 Business Standard report confirmed it now surpasses the combined reserves of the world's ten largest central banks. And of all of that, roughly 10% is formally pledged in the organised lending system today.

The rest isn't moving. It's dead capital!

In the 6+ years since of indiagold, the thing I've found most surprising isn't about gold. It's about why the money won't move. Why families that desperately need credit won't touch their gold even when the product in front of them is better, cheaper, and faster than anything available before. Maybe the answer isn't the loan. It's the infrastructure around it?

The locker problem that needs to be quantified

Almost all of India's household gold is stored at home. Not because people prefer it that way — because there's nowhere else to put it.

There are approximately 6 million bank lockers in India. By 2030, an estimated 60 million urban households will need secure storage. That gap — 54 million lockers — isn't going to be filled by the existing banking system. And the 6 million that exist come with conditions: long waitlists, mandatory liability products from the same bank, branch hours, steep annual rentals.

Here's the part that rarely comes up: banks are not obligated to insure the contents of your locker. RBI's own guidelines make this explicit — in a negligence case, the maximum compensation is 100 times the annual locker rent. A family paying ₹3,000 a year gets ₹3 lakh in compensation. The average Indian family stores multiples of that in the same box. No insurance. No recourse.

So what's the rational choice? Keep it home. And then live with what that means.

In October 2024, thieves broke into the SBI branch in Nyamati, Karnataka — gas cutter through the strongroom, 17.7 kg of customers' gold ornaments gone. In December 2024, six lockers were drilled open overnight at a Union Bank branch in Surat after CCTV cables were cut. In March 2025, a woman in Bengaluru opened her SBI locker to find 145 grams missing — a bank employee later arrested. Around the same time, a different bank employee in Bengaluru was found to have stolen 2.7 kg of gold from customer lockers to fund a gambling habit.

These are not isolated incidents. The formal safe-keeping infrastructure India has built for gold has a supply problem, an affordability problem, and — for the lockers that do exist — an insurance problem. That Godrej almirah at home, whatever its flaws, is at least always there.

The real barrier isn't awareness

The gold loan industry has spent enormous amounts on education campaigns. National print. Celebrity endorsements. The message: gold loans are good, use them.

Here's what those campaigns have never addressed: the people who don't take gold loans aren't avoiding them because they don't know about them. They're avoiding them because the experience requires surrendering privacy.

You walk into a branch and someone from your neighbourhood sees you. They know why you're there. Or you call for doorstep service and a stranger comes into your home, sees the jewellery, learns what you own and where it's kept. The social dynamics around pledging family gold — jewellery that carries significant emotional weight, often passed down through generations — are real. Any operator who's spent serious time with customers in this category understands this.

The unorganised sector holds roughly 65% of the gold loan market. Moneylenders charging 36–60% per annum. They shouldn't win on price. They win on speed, zero documentation, and absolute discretion. People will pay a 3x premium to avoid having to explain themselves to a stranger. That might seem like irrational behaviour but that's also customers telling you exactly what they need.

Why a better loan product can't solve this

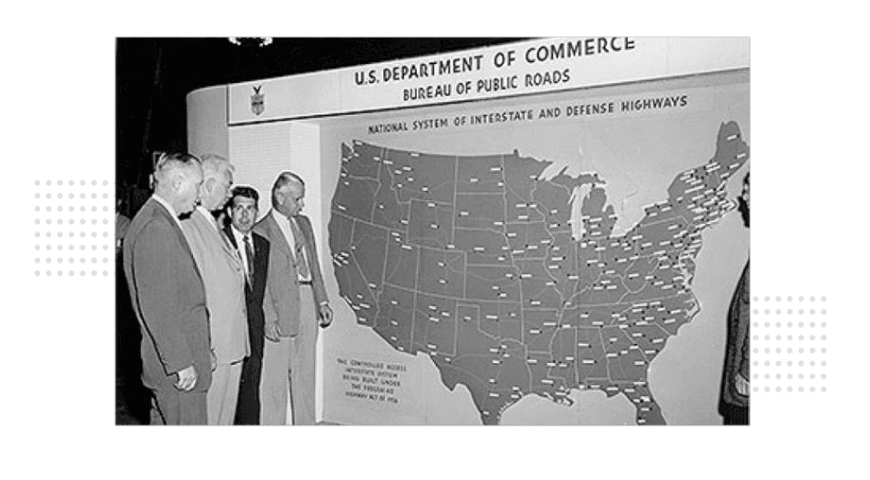

Our product head Ravish made this analogy.

“In 1956, the Eisenhower administration built 41,000 miles of interstate highway — originally for military evacuation logistics in the event of a Soviet strike. What actually happened was the American automobile boom. The highway unlocked demand that existed but had no infrastructure to express itself through. Ford, GM, and Chrysler could have kept making better cars. Without the road, the market size stays fixed. The highway expanded the market itself.”

The gold loan market is at exactly that inflection point.

Every improvement in the loan product operates within a constrained market. The constraint isn't the loan — it's that the gold is stored in ways that make accessing it psychologically and logistically expensive. The physical exposure. The social visibility. No insurance. No standardised assaying. The almirah. Better product innovation doesn't move any of those constraints.

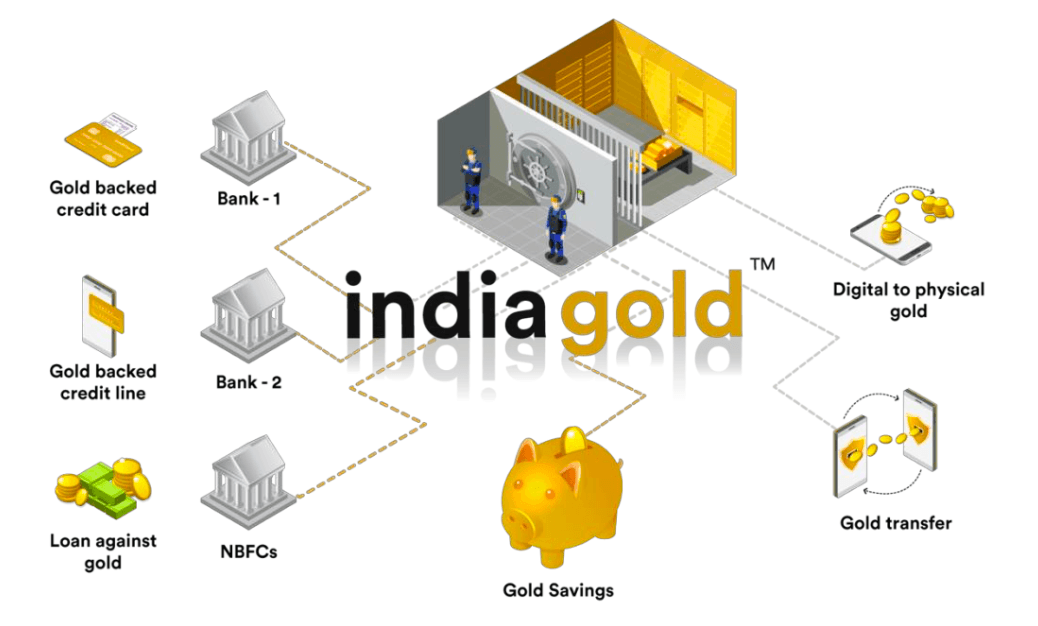

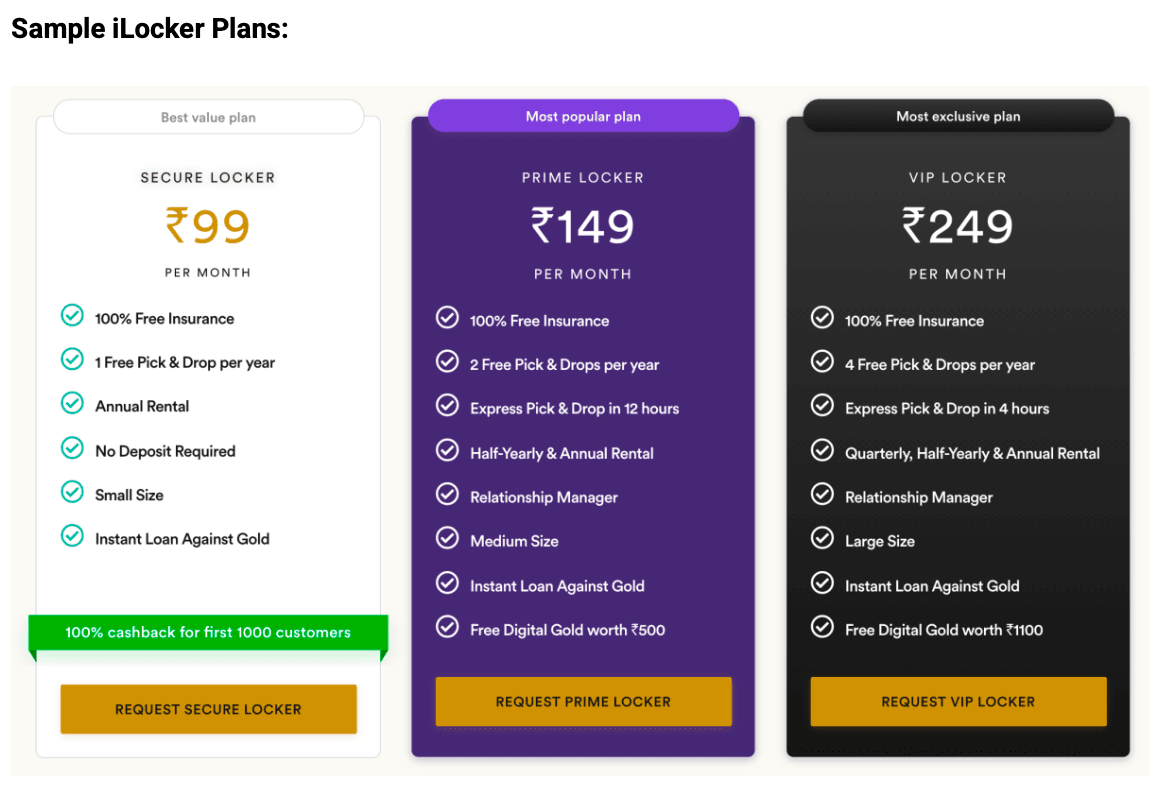

What unlocks the market is affordable, insured, accessible storage at scale — not the bank locker as it currently exists, but something meaningfully different. Doorstep pickup. Computer vision backed dual-assaying. Insurance included. Starting at ₹99 a month instead of ₹3,000 a year with a waitlist attached. That changes the calculus for tens of millions of families who currently have no viable option except the almirah.

What the locker actually enables

Once the gold is stored in a standardised, insured, assayed locker, something becomes possible that isn't possible today.

You take a loan against it from your phone. Nobody visits. The locker isn't opened. The gold isn't touched or moved. No new KYC. No documentation. Five minutes. The collateral is already verified, insured, and sitting in a vault with known weight and purity. Any partnering bank or NBFC can offer their best rate against it — because all the risk variables are transparent and controlled on their end.

More significantly: the locker balance becomes a credit identity.

India has 63 million micro and small enterprises. Over 99% are informal — no ITR, no GST history, no CIBIL footprint. They are creditworthy. They just can't prove it on paper. The same business owner who is invisible to every formal underwriting model almost certainly has gold at home. That gold, once stored and assayed, becomes an alternate financial identity. An API that tells any lender "this customer has 200 grams of 22-karat gold, assayed, insured, stored at X" is a credit score. The first real financial identity for customers the formal system has never been able to see.

The organised gold loan book stands at ₹15 lakh crore. The household gold stock it's drawing from is ₹350 lakh crore. That's not a penetration number that improves by making the loan marginally better. That's a penetration number that moves when the underlying infrastructure for storing and accessing gold changes fundamentally.

What the regulatory direction confirms

The RBI issued updated Directions on Lending Against Gold Collateral in June 2025. The revised LTV framework taking effect April 2026 is more generous for smaller borrowers — directly aligned with MSME use cases. The direction is clear.

What's also clear is where the limits of that direction sit. Regulation can expand what lenders can offer. It cannot solve the storage problem. It cannot build the 54 million missing lockers. It cannot remove the social cost of walking into a branch. It cannot give a family insurance on gold they're storing at home. Those are infrastructure problems — and they sit upstream of the loan entirely.

That's where we're focused at indiagold. Not just making the loan better. Building what the loan needs to sit on top of. A locker network that's affordable and accessible enough that the 90% of household gold currently sitting outside the formal system has somewhere safe to go — and a reason to move.

The gold loan market is growing. That's real and it will continue. But the market as it currently exists is a fraction of the market that's available. The gap between those two numbers isn't closed by a better app or a sharper rate sheet.

India's ₹350 lakh crore in household gold has been waiting for the right infrastructure for decades. The financial system is only now beginning to understand that the product was never the missing piece.

The writer is the co-founder of indiagold, a gold lending fintech with an NBFC license.

#indiagold #GoldLoan #Fintech #PersonalFinance #DigitalLending #GoldLoanAtHome #SmartFinancing #FinancialInclusion #InstantCredit #HassleFree #WorkingCapital #SMEFinance #BusinessGrowth