A Camera and a Model

𝗔𝗦𝗦𝗔𝗬𝗜𝗡𝗚 !!! Every gold lender talks about LTV caps as if they’re purely about regulatory limits and gold price volatility. In reality, in a branch-based model, LTV is often constrained by something else:

• 𝗔𝘀𝘀𝗮𝘆𝗲𝗿 𝘀𝗸𝗶𝗹𝗹 𝘃𝗮𝗿𝗶𝗮𝗻𝗰𝗲 (good assayers are rare, training takes time).

• 𝗦𝗮𝗹𝗲𝘀 𝗽𝗿𝗲𝘀𝘀𝘂𝗿𝗲 and “optimistic” carat calls to hit disbursal targets.

• 𝗘𝗺𝗽𝗹𝗼𝘆𝗲𝗲–𝗰𝘂𝘀𝘁𝗼𝗺𝗲𝗿 𝗰𝗼𝗹𝗹𝘂𝘀𝗶𝗼𝗻.

• 𝗖𝘂𝘀𝘁𝗼𝗺𝗲𝗿 𝗳𝗿𝗮𝘂𝗱 (plating, solder tricks, mixed alloys, hollow pieces).

• Also the uncomfortable truth: 𝗮𝘀𝘀𝗮𝘆𝗶𝗻𝗴 𝗶𝘀 𝗹𝗮𝗿𝗴𝗲𝗹𝘆 𝘃𝗶𝘀𝘂𝗮𝗹 𝗷𝘂𝗱𝗴𝗲𝗺𝗲𝗻𝘁 plus a loosely standardised process.

That combination creates an opaque, asynchronous decision chain. 𝗧𝗵𝗲 𝗽𝗲𝗿𝘀𝗼𝗻 𝘄𝗵𝗼 𝗯𝗲𝗻𝗲𝗳𝗶𝘁𝘀 𝗳𝗿𝗼𝗺 𝗮 𝗵𝗶𝗴𝗵𝗲𝗿 𝘃𝗮𝗹𝘂𝗲 𝗲𝘀𝘁𝗶𝗺𝗮𝘁𝗲 𝗶𝘀 𝗼𝗳𝘁𝗲𝗻 𝗰𝗹𝗼𝘀𝗲 𝘁𝗼 𝘁𝗵𝗲 𝗽𝗲𝗿𝘀𝗼𝗻 𝗺𝗮𝗸𝗶𝗻𝗴 𝘁𝗵𝗲 𝗲𝘀𝘁𝗶𝗺𝗮𝘁𝗲. Controls exist, but they are typically post-facto, sample-based, and easy to game.

So lenders do what any rational risk team would do: they tighten LTV. The irony is that the regulatory LTV buffer is already designed to cushion gold price fluctuations. But 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝗽𝘂𝗿𝗶𝘁𝘆/𝘃𝗮𝗹𝘂𝗮𝘁𝗶𝗼𝗻 𝗿𝗶𝘀𝗸 𝗶𝘀 𝗻𝗼𝗶𝘀𝘆, 𝗹𝗲𝗻𝗱𝗲𝗿𝘀 𝗮𝗱𝗱 𝗮 𝘀𝗲𝗰𝗼𝗻𝗱 𝗹𝗮𝘆𝗲𝗿 𝗼𝗳 𝗰𝗼𝗻𝘀𝗲𝗿𝘃𝗮𝘁𝗶𝘀𝗺. 𝗧𝗵𝗲 𝗰𝘂𝘀𝘁𝗼𝗺𝗲𝗿 𝗽𝗮𝘆𝘀 𝗳𝗼𝗿 𝗶𝘁.

And the pain shows up most in the segment that needs gold loans the most: self-employed borrowers seeking urgent working capital. Gold prices go up, but many customers still receive less than the maximum value their collateral can genuinely support—because t𝗵𝗲 𝘀𝘆𝘀𝘁𝗲𝗺 𝗰𝗮𝗻𝗻𝗼𝘁 𝘁𝗿𝘂𝘀𝘁 𝗶𝘁𝘀𝗲𝗹𝗳 𝘁𝗼 𝘃𝗮𝗹𝘂𝗲 𝗶𝘁 𝗮𝗰𝗰𝘂𝗿𝗮𝘁𝗲𝗹𝘆 𝗶𝗻 𝗿𝗲𝗮𝗹 𝘁𝗶𝗺𝗲.

The obvious fix (and why it won’t be the breakthrough). Yes, you can reduce discretion by deploying XRF and integrating it into the LMS so purity readings are captured directly, with audit logs and reduced scope for manual tampering.

It works. But it’s also capex-heavy, operationally demanding, and harder to scale across every branch, counter, and partner location at industry scale.

Which reminds me of payments circa 2015.

Back then, dozens of companies tried to “democratise” offline payments by building low-cost POS/EDC hardware. The less obvious answer was to use what was already ubiquitous: smartphones. That single decision unlocked QR rails and created what we now call UPI-scale distribution.

I think gold loans are staring at a similar pattern.

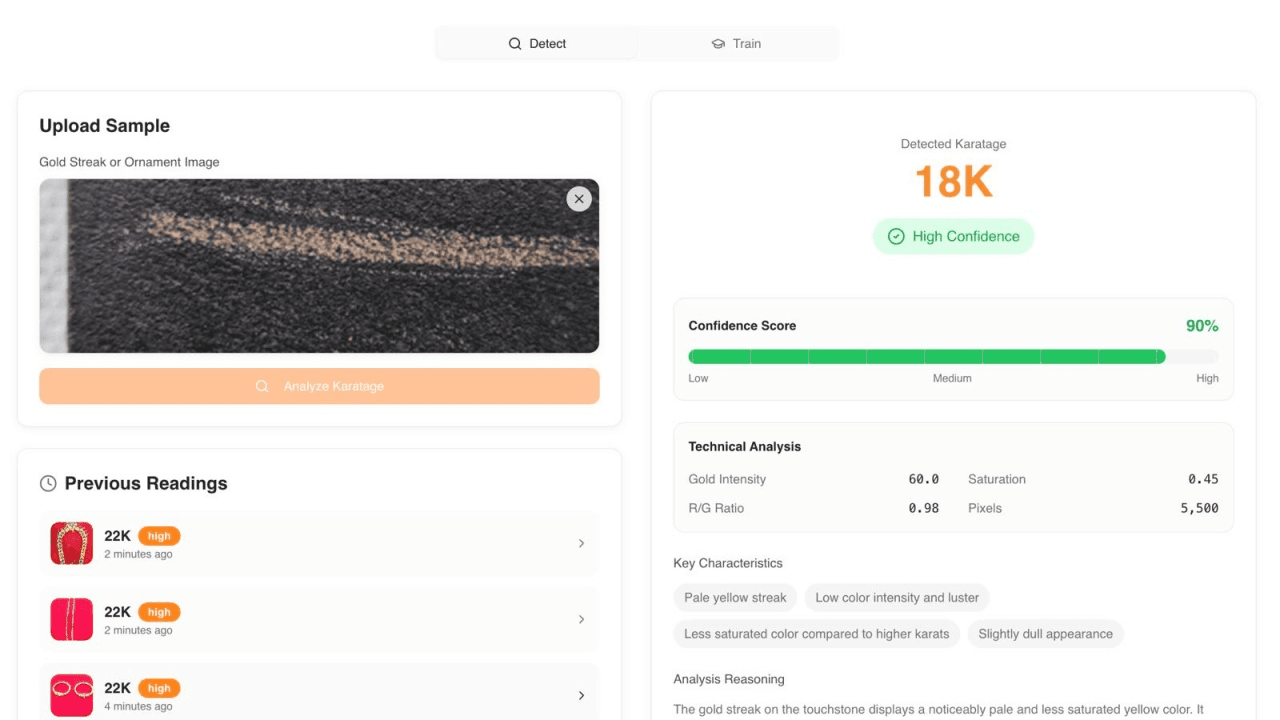

𝗧𝗵𝗲 “𝘀𝗺𝗮𝗿𝘁𝗽𝗵𝗼𝗻𝗲-𝗻𝗮𝘁𝗶𝘃𝗲” 𝗮𝗽𝗽𝗿𝗼𝗮𝗰𝗵 𝘁𝗼 𝗮𝘀𝘀𝗮𝘆𝗶𝗻𝗴.

Every assayer already has a smartphone. And assaying—especially touchstone + acid workflows—has a large visual and temporal component: streak formation, reaction timing, colour change, dissolution patterns.

A 𝗽𝗿𝗼𝗽𝗲𝗿𝗹𝘆 𝘁𝗿𝗮𝗶𝗻𝗲𝗱 𝗰𝗼𝗺𝗽𝘂𝘁𝗲𝗿 𝘃𝗶𝘀𝗶𝗼𝗻 𝗺𝗼𝗱𝗲𝗹 (ideally video-based, protocol-driven, and calibrated for lighting) can materially reduce:

• 𝗦𝗸𝗶𝗹𝗹 𝗱𝗲𝗽𝗲𝗻𝗱𝗲𝗻𝗰𝗲 (standardising interpretation)

• 𝗜𝗻𝘁𝗲𝗻𝘁 𝗿𝗶𝘀𝗸 (constraining discretionary valuation)

• 𝗦𝗽𝗲𝗲𝗱/𝗧𝗔𝗧 𝘃𝗮𝗿𝗶𝗮𝗻𝗰𝗲 (fast, consistent outputs)

• 𝗙𝗿𝗮𝘂𝗱 𝘃𝗲𝗰𝘁𝗼𝗿𝘀 (flagging anomalies, forcing “manual/XRF required” paths)

• and most importantly, 𝗼𝘃𝗲𝗿-𝘃𝗮𝗹𝘂𝗮𝘁𝗶𝗼𝗻 𝘁𝗮𝗶𝗹 𝗿𝗶𝘀𝗸, which is what drives lenders to tighten LTV in the first place

𝗧𝗵𝗶𝘀 𝗶𝘀 𝗻𝗼𝘁 𝗮𝗯𝗼𝘂𝘁 𝗿𝗲𝗽𝗹𝗮𝗰𝗶𝗻𝗴 𝗮𝘀𝘀𝗮𝘆𝗲𝗿𝘀. 𝗜𝘁’𝘀 𝗮𝗯𝗼𝘂𝘁 𝗺𝗼𝘃𝗶𝗻𝗴 𝗳𝗿𝗼𝗺 “𝘁𝗿𝘂𝘀𝘁 𝘁𝗵𝗲 𝗶𝗻𝗱𝗶𝘃𝗶𝗱𝘂𝗮𝗹” 𝘁𝗼 “𝘁𝗿𝘂𝘀𝘁 𝘁𝗵𝗲 𝗽𝗿𝗼𝗰𝗲𝘀𝘀 + 𝘁𝗲𝗹𝗲𝗺𝗲𝘁𝗿𝘆 + 𝗮𝘂𝗱𝗶𝘁𝗮𝗯𝗶𝗹𝗶𝘁𝘆”.

In lending terms, the 𝗺𝗼𝗱𝗲𝗹 𝗱𝗼𝗲𝘀𝗻’𝘁 𝗻𝗲𝗲𝗱 𝘁𝗼 𝗯𝗲 𝗽𝗲𝗿𝗳𝗲𝗰𝘁. It needs to be asymmetrically safe: calibrated to avoid overestimating purity, produce conservative lower bounds when uncertain, and automatically trigger maker-checker or XRF escalation for edge cases.

𝗪𝗵𝗮𝘁 𝘄𝗲 𝗹𝗲𝗮𝗿𝗻𝗲𝗱 𝗯𝘂𝗶𝗹𝗱𝗶𝗻𝗴 𝘁𝗵𝗶𝘀 𝗮𝘁 𝗶𝗻𝗱𝗶𝗮𝗴𝗼𝗹𝗱

𝗙𝗶𝘃𝗲 𝘆𝗲𝗮𝗿𝘀 𝗮𝗴𝗼 𝗮𝘁 𝗶𝗻𝗱𝗶𝗮𝗴𝗼𝗹𝗱, 𝘄𝗲 𝗶𝗺𝗽𝗹𝗲𝗺𝗲𝗻𝘁𝗲𝗱 𝗰𝗲𝗻𝘁𝗿𝗮𝗹𝗶𝘀𝗲𝗱, 𝗿𝗲𝗮𝗹-𝘁𝗶𝗺𝗲 𝗺𝗮𝗸𝗲𝗿-𝗰𝗵𝗲𝗰𝗸𝗲𝗿 𝗳𝗼𝗿 𝗮𝘀𝘀𝗮𝘆𝗶𝗻𝗴—something that is still surprisingly not widespread in a very large gold loan industry.

That alone reduced discretion and improved consistency, because valuation stopped being a branch-local, post-facto activity.

In parallel, we began training our own CV tooling. At the time, capabilities were early and deployment constraints were real.

Today, the stack is different.

With a robust assaying protocol, centralised real-time controls, and modern CV models, you can get close to something the industry has struggled with for decades:

Maximum value to the customer, with better unit economics and lower fraud/NPAs for the lender.

The “UPI moment” for gold loans may not be a new product. It may simply be this:

𝗠𝗮𝗸𝗶𝗻𝗴 𝗴𝗼𝗹𝗱 𝘃𝗮𝗹𝘂𝗮𝘁𝗶𝗼𝗻 𝘁𝗿𝘂𝘀𝘁𝗲𝗱, 𝗳𝗮𝘀𝘁, 𝗮𝗻𝗱 𝘀𝗼𝗳𝘁𝘄𝗮𝗿𝗲-𝗻𝗮𝘁𝗶𝘃𝗲—𝗮𝘁 𝘁𝗵𝗲 𝗲𝘅𝗮𝗰𝘁 𝗽𝗼𝗶𝗻𝘁 𝘄𝗵𝗲𝗿𝗲 𝗺𝗼𝗻𝗲𝘆 𝗶𝘀 𝗱𝗶𝘀𝗯𝘂𝗿𝘀𝗲𝗱.

If we can do that, LTV stops being a conservative blunt instrument and starts becoming what it was supposed to be: a rational buffer for market risk, not a hedge against process risk.

Gold loans are often called the last-mile credit product for Bharat. If we can solve assaying at scale, we unlock the ability to deliver maximum value to customers while simultaneously improving portfolio quality and unit economics.

That's a rare alignment of customer benefit and business outcome.

𝗧𝗵𝗲 𝗨𝗣𝗜 𝗼𝗳 𝗴𝗼𝗹𝗱 𝗹𝗼𝗮𝗻𝘀 𝘄𝗼𝗻'𝘁 𝗯𝗲 𝗮 𝗽𝗮𝘆𝗺𝗲𝗻𝘁 𝗿𝗮𝗶𝗹. 𝗜𝘁 𝗺𝗶𝗴𝗵𝘁 𝗷𝘂𝘀𝘁 𝗯𝗲 𝗮 𝗰𝗮𝗺𝗲𝗿𝗮 (and a model).

GLAAS (gold loan as a service)

#ComputerVision #AI #FintechInnovation #DeepTech #IndiaFintech #Fintech #GoldLoans #ComputerVision #StartupIndia #Lending