You can’t underwrite someone who doesn’t exist...

When an industry stalwart like Mr. Nirmal Jain says the "gold loans function as working capital for micro-enterprises", it helps validate why we started indiagold in 2020 - to build the most accessible, affordable & flexible working capital product for small business owners. Though I differ on need for thousands of physical branches as I believe it's more of incumbents inertia than catering to evolving customer needs & letting technology address challenges, than people.

Between my co-founder Deepak Abbot & I, we've invested the last 5+ years & perhaps 23,000 hours each (Malcom Gladwell analogy) in doing ONE SINGLE THING - understanding gold loans (customers, suppliers, asset-class, regulations, product, technology, logistics, challenges, cycles). And the most surprising thing I’ve learned in that time isn’t about gold. It’s about credit. Specifically, who gets it, who doesn’t, and why the gap between those two groups has stubbornly refused to close.

Let me lay out the picture as I see it.

How India actually runs India has approximately 63 million micro and small enterprises. They contribute 30.1% of GDP, account for 45.73% of total exports, and employ over 200 million people. If you stripped MSMEs out of the economy, India wouldn’t just slow down — it would stop.

But here’s what that 63 million number obscures: over 99% of these businesses are micro enterprises. The kirana owner. The small-scale fabricator. The embroidery unit. The roadside caterer supplying tiffins to offices. The single-truck transporter. These are not startups. They’re not formalised. Most of them don’t file income tax returns, don’t have GST histories, and don’t have credit bureau footprints. They run on cash, relationships, and word of mouth.

They are the real India — and they are almost entirely underserved by the formal credit system.

The credit gap is structural, not accidental

SIDBI estimates India’s addressable MSME credit gap at ₹30 lakh crore — nearly 24% of the sector’s total debt demand. Only about 20% of MSMEs have any access to formal credit, and that number has improved only modestly over the past decade.

This is not a pipeline problem. It’s not that banks are too few, or that branch networks haven’t expanded.

The problem is that the bank loan — as a product — was designed for a very specific customer: one with audited financials, GST compliance, a CIBIL score, and collateral the system recognises.

The typical micro enterprise owner has none of these. They may be doing ₹40–50 lakh in annual revenue — entirely in cash. No ITR. No clean books. No fixed assets in their name. They’re not unbankable because they’re unviable. They’re unbankable because the underwriting architecture of formal credit was never built with them in mind.

And even when formal products nominally exist for them — MUDRA loans, CGTMSE-backed credit — the friction kills them at execution. A bank business loan takes 4–8 weeks to process, assuming complete documentation. An MSME owner who needs ₹1.5 lakh tomorrow to pay a supplier and capture an inventory deal doesn’t have 4 weeks.

What they actually do instead In the absence of formal credit, MSMEs borrow from wherever they can. And wherever they can is, more often than not, expensive and predatory.

Informal moneylenders charge anywhere from 36% to 60% per annum — with rural markets seeing rates that go higher. Supplier credit comes with dependency and margin compression. Rotating chit funds help with lump-sum needs but can’t meet working capital timing precisely. And personal savings — the most common backstop — quietly cannibalises the household balance sheet.

These aren’t just expensive alternatives. They’re structurally coercive. The moneylender’s enforcement mechanism isn’t a legal notice — it’s social pressure, local networks, and sometimes property seizure. Debt traps are common. The micro entrepreneur either overpays for money or starves the business of the capital it needs to grow. Both outcomes compound over time.

MUDRA has disbursed over ₹32 lakh crore cumulatively since 2015, across more than 52 crore loan accounts. That’s significant government intent, and the scheme’s upper limit was recently raised to ₹20 lakh. But the reach into truly informal micro enterprises — those without any bureau footprint — remains shallow. You can’t underwrite someone who doesn’t exist in the data infrastructure.

And then there’s gold India’s households hold approximately 25,000 tonnes of gold — the largest private gold stock in the world. At today’s 22-karat prices, that’s approximately ₹350 lakh crore in household wealth. This gold wasn’t accumulated by the rich. It was accumulated, gram by gram, across generations of middle-income and lower-middle-income families — bought at weddings, gifted at births, purchased as savings when there was no other savings instrument people trusted.

Now here’s the thing that makes this interesting from a credit standpoint: the same MSME owner who has no ITR, no GST filing, no CIBIL score — almost certainly has gold at home. This isn’t coincidence. It’s centuries of financial behaviour. Gold in India functions simultaneously as jewellery, savings, insurance, and — when designed correctly — collateral.

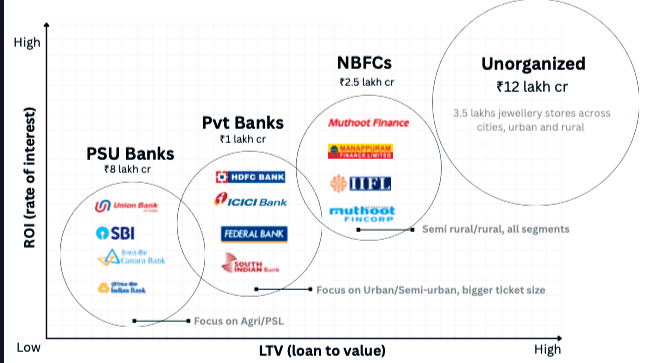

Of that 25,000-tonne stock, only around ~10% is formally pledged in the organised sector today. The organised gold loan market — NBFCs plus banks — has crossed ₹15 lakh crore and is growing at 30%+ annually. Against ₹350 lakh crore in household gold wealth, that penetration is extraordinarily low. The headroom is real.

Why gold loans fit MSMEs better than any other credit product A gold loan is the anti-bank-loan — in the best sense.

No income proof. No credit history. No business vintage. No end-use restriction. No 6-week process. You bring in your gold, it gets assayed and weighed, and you receive up to 75–85% of its market value as a loan, depending on ticket size — per RBI’s revised LTV framework effective April 2026. In a branch, this takes 30–45 minutes. At indiagold, we’ve taken it to the customer’s doorstep and compressed it further.

The repayment structure is equally well-suited. Gold loans are typically interest-serviced monthly, with principal repaid at maturity or in bullet. For an MSME owner with lumpy, irregular cash flows — whose revenue comes in when the order is fulfilled, not on the 1st of every month — this is precisely the structure they need. They’re not servicing a large EMI on a date that may or may not align with their receivables.

The cost is rational. Organised gold loan lenders — regulated NBFCs — lend at 10–18% per annum. That’s a fraction of the moneylender rate. And the downside scenario is bounded: if you cannot repay, the lender recovers from the pledged gold. There’s no personal guarantee, no third-party coercion, no asset seizure beyond the collateral already in the lender’s custody. The risk is transparent and contained — for both sides.

CRIF High Mark data shows gold loans grew 34.6% year-on-year in Q1FY26, leading all consumption loan categories in India by a wide margin. The delinquency profile of gold loans is structurally better than unsecured MSME lending — because collateral disciplines both borrower behaviour and lender underwriting. The organised gold loan book has crossed ₹15 lakh crore, and it is still growing.

The regulatory and government alignment Gold loan NBFCs are not a grey market. They operate under a clear, well-defined RBI regulatory framework — LTV caps, auction norms, KYC requirements, and capital adequacy standards. In June 2025, RBI issued updated Directions on Lending Against Gold Collateral, introducing a tiered LTV structure that is more generous for smaller borrowers — directly aligned with the MSME use case.

Successive Union Budgets have identified MSME credit access as a priority. The JAM (Jan Dhan–Aadhaar–Mobile) stack has created infrastructure for digital KYC and rapid disbursement. Gold loan digitisation — which is what indiagold is building — sits precisely at the intersection of government intent and ground-level financial behaviour.

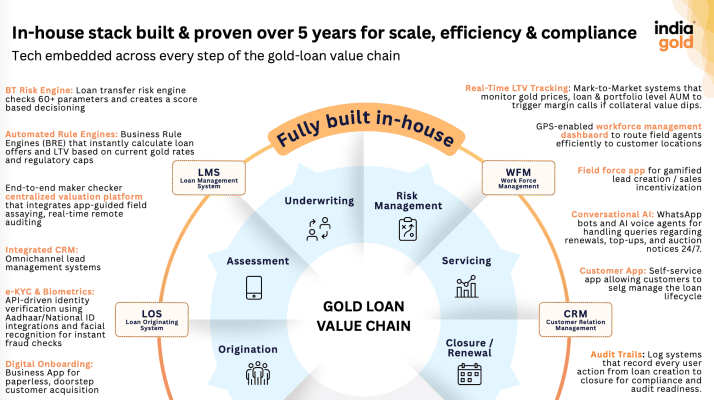

What we’re building at indiagold indiagold is a gold lender purpose built for the self-employed.

Our proprietary tech stack delivers higher than market loan amounts, safer loan transfers & product differentiation unmatched in the market. Our performance proved our thesis - that technology can fundamentally improve traditional and unorganised gold lending through an asset-light model.

We started indiagold with a thesis that has only gotten stronger: India’s micro entrepreneurs are creditworthy. They just cannot prove it on paper. Gold removes that requirement entirely. The collateral is the underwriting.

We’ve built a platform that brings the gold loan to the customer — at their home or business — without requiring a branch visit, paperwork marathons, or documentation they don’t have. Our MSME borrowers use the funds for supplier payments, inventory build, equipment, and working capital bridge — the exact short-duration, recurring credit needs that no formal product efficiently meets at this ticket size.

The renewal rate tells us something important: when an MSME owner gets a gold loan and uses it to grow the business, they come back. The credit product fits the cash flow. The trust gets built. And the relationship deepens.

If you’re looking at MSME credit in India, here’s how I’d think about the landscape:

Banks have the intent but not the product fit. Their underwriting models don’t work for informal micro enterprises, and PSB balance sheets are still working through prior MSME NPA cycles.

Unsecured fintech lenders are hitting headwinds — rising defaults, RBI tightening on personal loan products, and the fundamental challenge of underwriting customers with thin or fabricated data.

Gold loans are backed by a tangible, universally liquid asset. The underwriting doesn’t depend on data that may or may not exist.

The repayment structure matches MSME cash flow reality. The cost to the borrower is dramatically lower than alternatives.

And the asset base — ₹350 lakh crore in household gold, less than 10% pledged in the organised sector — gives the market a structural growth runway that few credit categories can match.

This isn’t a workaround product for a hard-to-serve customer segment. It’s the right product for this customer — built around the assets they actually hold and the cash flow reality they actually live in.

India’s MSMEs have been carrying the answer around their necks for generations. The financial system is only now beginning to catch up.

#indiagold #GoldLoan #Fintech #PersonalFinance #DigitalLending #GoldLoanAtHome #SmartFinancing #FinancialInclusion #InstantCredit #HassleFree #WorkingCapital #SMEFinance #BusinessGrowth