India Trusts Its Gold. Its Gold Lenders Don't.

India’s Complicated Relationship with Gold

India holds more privately owned gold than any other country on earth. Estimates from the World Gold Council place Indian household holdings at roughly 25,000 tonnes, with some modelling approaches putting the number closer to 30,000 tonnes. These are not census counts — they are estimates derived from import flows, recycling data, and consumption modelling — but the broad conclusion is widely accepted: Indian households collectively hold an enormous amount of gold.

Most of that gold sits in jewellery — bangles, chains, necklaces, coins, and heirloom pieces accumulated over generations. For many families it functions as a form of savings and emergency collateral.

The gold is trusted, inherited, and rarely tested however that changes the moment someone walks into a gold loan branch.

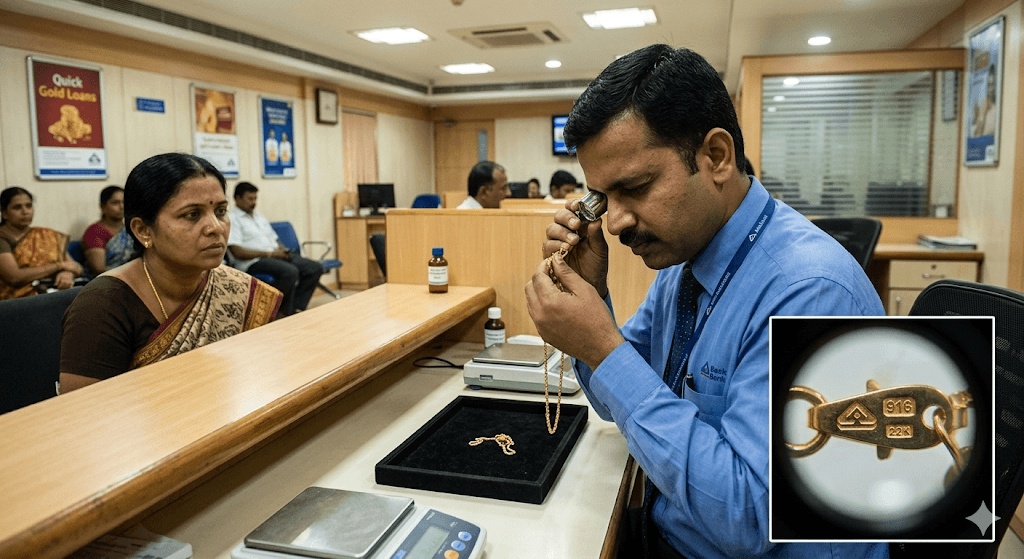

Majority is misinformed about the quality of their gold. Most customers believe their jewellery is either 24 karat or 22 karat & they feel cheated when their gold gets tested in front of them.

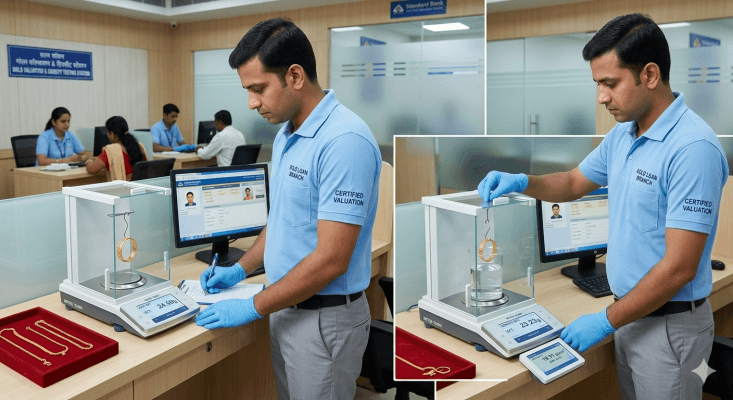

India’s organised gold loan market — served by NBFCs, banks and cooperative institutions — has grown into a market worth more than ₹15 lakh crore in outstanding loans. What allows such a large system to function is a process that happens quietly at the branch counter before any money is disbursed: assaying the gold.

These figures cover only the organised, regulated sector. An informal gold lending market — unregistered moneylenders and local pawnbrokers operating outside the regulatory perimeter — accounts for an estimated 60 percent of total gold lending in India. Documentation standards, assaying practices, and borrower protections vary widely in this segment.

Before a lender releases funds, two questions must be answered:

- Is this actually gold jewellery?

- How much gold is really in it?

The methods used to answer those questions combine metallurgy, chemistry, and something less formal but equally important — experience.

What “Assaying” Means in a Gold Loan Context

In strict metallurgical terms, assaying refers to determining the exact composition of a metal using laboratory methods such as fire assay. Gold loan branches are not laboratories. The objective here is different.

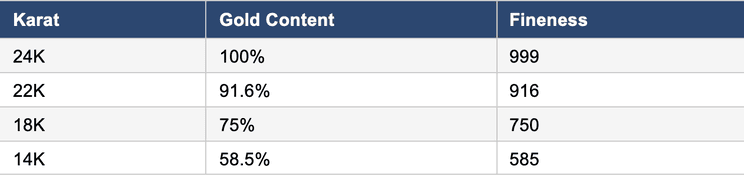

The goal is rapid, reliable screening of jewellery to estimate purity and detect fraud. Gold purity is typically expressed in karats:

Traditional Indian jewellery is usually 22 karat, while modern studded or designer jewellery often uses 18 karat. However, jewellery is rarely a simple piece of metal. Most pieces contain:

- solder joints

- stones and enamel work

- hollow sections

- mixed alloys

This means assaying is not about measuring a single metal sample — it is about estimating the effective gold content of a complex object.

The Practical Assaying Process in Gold Loan Branches

In most branches the process follows a layered sequence of checks. No single test is decisive; each step filters out different kinds of risk.

1. Visual inspection and hallmark verification The appraiser first examines the jewellery for hallmarks issued by the Bureau of Indian Standards. BIS hallmarking became mandatory for gold jewellery sold by registered jewellers in June 2021, covering 14, 18, and 22 karat. Coverage was extended to include 9 karat from July 2025.

The physical BIS hallmark stamp carries four components:

- the BIS triangular mark

- the purity number (916, 750, etc.)

- the Assaying and Hallmarking Centre mark

- a jeweller identification mark

Additionally, since June 2021 each hallmarked piece carries a Hallmark Unique Identification — a six-digit numeric code registered in the BIS digital database. The HUID can be verified using the BIS Care app or BIS portal, which retrieves the full hallmarking record: which centre tested the piece, when, and at what declared fineness.

A hallmark is a strong positive signal, but it is not treated as definitive. Hallmarks can be forged, and purity can change if jewellery has been repaired or modified after hallmarking. The appraiser also looks for structural cues:

- solder joints

- colour variations

- unusual wear patterns

- signs of plating

These visual signals often determine how cautiously the next steps are conducted.

2. Weight, structure and density cues An experienced assayer evaluates how the jewellery feels relative to its size. Gold is a dense metal, but jewellery fraud frequently involves structural manipulation rather than metallurgical trickery. Common issues include:

- hollow bangles

- internal rods or filler metals

- wax-filled ornaments

Weight-to-volume mismatches can reveal these problems quickly. Branches sometimes also perform simple checks such as:

- tapping pieces to detect hollowness

- examining seam lines or caps

- using small magnets to detect hidden steel pins

These are not definitive tests, but they are effective early filters.

Rare (haven't seen this used in gold lending): Some trained appraisers may also perform a specific gravity test based on the Archimedes principle: weigh the piece in air, then weigh it while fully submerged in water. Specific gravity equals the weight in air divided by the difference between the air weight and the submerged weight. The specific gravity test reliably detects hollow construction and base-metal cores. It has practical limitations on complex pieces: embedded stones, enamel, hollow sections, and solder joints all distort the reading. Most appraisers use it selectively on plain metal items — coins, bars, simple bangles — rather than on heavily assembled jewellery.

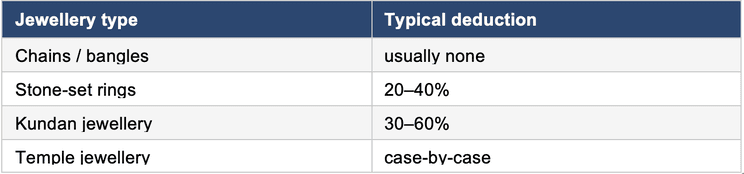

3. Stone and non-gold deductions Loans are issued only against net gold weight, so stones and non-gold components must be deducted. In practice, branch appraisers rely on experience-based heuristics rather than precise weighing of each stone. Typical branch deductions might look like this:

Very small stones are often ignored if their weight is negligible. These deductions are recorded before valuation and explained to the borrower.

4. The touchstone test The central diagnostic tool in most Indian gold loan branches is the touchstone test.

The jewellery is rubbed against a black stone (traditionally lydite), leaving a metallic streak. Reference alloys of known purity are rubbed beside it. Nitric acid is then applied. Nitric acid dissolves base metals like copper and silver but leaves gold largely unaffected. By comparing the reactions of the streaks, the appraiser estimates purity.

For high-karat pieces — 22K and above — concentrated nitric acid alone may not produce a clear diagnostic reaction. Gold’s resistance to nitric acid is what defines it. For these pieces, appraisers use aqua regia: one part nitric acid to three parts hydrochloric acid, which can dissolve even 24K gold. Comparing how the test streak dissolves relative to reference streaks under aqua regia allows discrimination at the high end of the karat range.

Touchstone testing is typically accurate to about ±1–2 karats, which is sufficient for lending decisions.

Experienced appraisers often take multiple streaks from different parts of a piece, since solder joints or surface wear can affect readings.

5. Direct acid testing & cuts Rare: If needed, the appraiser may scratch a tiny area of the jewellery and apply acid directly to the exposed metal. This helps detect:

- thick plating

- layered construction

- inconsistent alloy composition The mark is small but technically destructive.

Similarly, tiny cuts are made in certain type of jewellery to ascertain composition beyond surface.

The Often-Ignored Factor: Solder

Many jewellery pieces contain numerous solder joints. These joints are made with alloys of lower gold purity than the main metal.

Until a government ban effective January 2016, the standard solder used by most Indian goldsmiths was KDM — a cadmium-gold alloy. KDM solder typically ran at 16 to 18 karat, well below the 22K purity of the surrounding metal. A piece that is 22K in its body but joined at multiple points with KDM solder can have an effective overall purity closer to 20K, depending on the proportion of solder to metal. Cadmium also contaminates a gold melt at the refinery stage and must be refined out at cost.

Post-2016, jewellers shifted to silver-based or gold-based solder alternatives that more closely match the purity of the base metal. However, pieces manufactured or repaired before 2016 remain in active circulation in the pledged gold market. Experienced appraisers account for KDM dilution when estimating purity on heavily assembled pieces — particularly temple jewellery, kundan work, and older necklaces with multiple repair points.

Complex necklaces may contain dozens of solder points. These joints collectively dilute the overall gold content of the piece. A seasoned appraiser treats visible solder as a reason to be conservative in the purity estimate, not to ignore it.

Regional Alloy Variation

The non-gold portion of Indian 22K jewellery is not standardised across regions. The copper-to-silver ratio in the alloying metals varies by jewellery tradition, and these differences affect how pieces behave on both the density test and the touchstone.

South Indian temple jewellery and Kerala-style thick bangles typically use copper-dominant alloys that sit at the lower end of the density range for 22K. Rajasthani kundan work involves specific structural alloys built around a lac core with gold foil layers. Bengali jewellery traditions have characteristic alloy compositions with distinct touchstone streak behaviour under acid. These are not defects — a piece can be correctly 916 fine and still behave differently on the touchstone depending on its regional origin.

An appraiser trained primarily on one regional jewellery style may initially misread pieces from another region. Major gold loan NBFCs address this through training programmes that expose appraisers to a wide range of jewellery styles and regional alloy signatures before deployment.

At indiagold, our centralised assaying and credit tools eliminate regional or person-dependant variables.

Why XRF Machines Are Not Used Everywhere

Modern X-ray fluorescence (XRF) analysers can determine elemental composition within seconds. Desktop machines can cost roughly ₹8–12 lakh per unit when procured at scale for institutional deployment. For a lender operating thousands of branches, deploying these everywhere would require several hundred crore rupees in capital expenditure. But cost alone does not explain their limited use.

The real limitation is what XRF actually measures.

The surface analysis problem

XRF measures the elemental composition of the outer surface layer of a metal. In gold alloys, its effective penetration depth is typically 10–50 microns. That means XRF provides very accurate surface karatage, but says little about the internal structure of the object. This creates several potential blind spots:

- thick gold plating over base metal cores

- hollow jewellery with internal fillers

- gold-cased objects with different internal metals

- multi-layer construction in traditional jewellery

Detecting internal composition reliably would require destructive fire assay or advanced technologies such as CT scanning — neither of which is practical in a retail lending branch.

Operational constraints

Branch-level operations introduce additional challenges:

- high staff turnover

- need for regular calibration using reference standards

- environmental sensitivity of instruments

- maintenance and repair costs

A dropped handheld XRF unit can require expensive servicing. Maintaining laboratory discipline across thousands of branches is operationally difficult.

Where XRF Does Fit

XRF is not absent from the industry. It is widely used in:

- refinery testing

- gold buying operations

- centralised appraisal hubs

- high-value branches

In these settings, XRF works best as a supplementary verification tool, not the sole basis for lending decisions.

Why Traditional Assaying Still Works Despite sounding old-fashioned, the touchstone + acid method remains well suited to gold lending. The reason is simple: the objective is fraud detection, not laboratory-grade purity measurement. Experienced appraisers evaluate multiple signals simultaneously:

- weight relative to volume

- structural construction

- solder patterns

- acid reactions

- hallmark authenticity

These physical cues often reveal anomalies that surface-analysis machines cannot detect.

A skilled appraiser handling dozens of pieces daily develops a strong pattern-recognition ability — identifying unusual alloys, suspicious construction techniques, or regional jewellery styles.

How This Differs: Jewellers, Cash-for-Gold, and Regulated Lenders

Gold assaying happens in three distinct commercial contexts in India. The tools overlap, but the incentives and accountability structures are completely different.

Jewellers A jeweller buying old gold at the counter is transacting at or near market price. Every rupee of error in the purity assessment comes directly out of their margin or goes into it. They have a direct financial interest in the outcome.

Most jewellers use the touchstone and acid test, the same method used by gold loan branches. The difference is what surrounds it. The jeweller’s assessment is undocumented, unaudited, and unregulated. The customer, having sold the jewellery outright, has no recourse if the reading was wrong or deliberately conservative. An intentional underestimation of purity by two karats is worth real money to a jeweller buying in volume.

KDM solder affects jewellers differently from lenders. When a jeweller melts down old jewellery, cadmium from KDM joints contaminates the melt and must be refined out. This is a known cost that experienced jewellers factor into their buying price for pre-2016 assembled pieces — another reason purity estimates from jewellers on complex pieces skew low.

Cash-for-Gold Counters Cash-for-gold operators work with the strongest financial incentive to undervalue of anyone in the gold assessment chain. The entity doing the assessment is also the entity paying for the gold. Every rupee shaved off the purity estimate is margin retained.

Many cash-for-gold counters use XRF machines, partly for speed and partly because the equipment looks authoritative to customers who are unfamiliar with the penetration depth limitation. An XRF result printed on a slip of paper feels definitive. The customer typically has no way to challenge it.

There is no documentation requirement, no third-party verification, and no regulatory oversight of the assaying process at a cash-for-gold counter. The customer’s only protection is their own knowledge.

Regulated Lenders A regulated lender’s assayer occupies a structurally different position. They are an employee, not a buyer. Their job is to protect the institution from fraudulent collateral while accurately serving the borrower. They have no financial interest in the outcome of the purity assessment.

The customer retains ownership of the jewellery throughout the loan tenure. The gold is stored, not melted or sold. This creates a different relationship between the assayer and the asset: the goal is an accurate number, not a favourable one.

The borrower also has a direct interest in accurate assaying. An underestimate of purity means a smaller loan than the collateral justifies. The RBI’s 2025 Directions reinforce this through mandatory borrower presence during assaying, documented deduction certificates, and a requirement that all deductions be explained to the customer before the loan is sanctioned. These obligations apply identically to banks, NBFCs, cooperative banks, and housing finance companies — the entire regulated sector.

This combination — no personal financial stake, trained staff, documentation requirements, and regulatory oversight — makes the regulated lender’s assaying process the most accountable of the three. It is not necessarily the most precise, but it is the most structurally honest.

The Role of Loan-to-Value Limits

The gold loan system also includes a structural safeguard: conservative loan-to-value (LTV) limits imposed by the Reserve Bank of India.

Under the RBI’s Lending Against Gold and Silver Collateral Directions, 2025, maximum LTV ratios are:

These limits protect lenders from market volatility but also provide a buffer against moderate assaying error. If purity is overestimated slightly — for example assessing an 18K piece as 20K or 22K — the loan amount generally remains covered by the underlying gold value. Losses arise primarily when jewellery is fundamentally misrepresented, not when purity estimates differ by a karat or two.

The nominal 25% buffer at 75% LTV is thinner in practice than it appears on paper. Gold sold at default auction typically realises 92–97% of melt value — buyers price in refining costs and residual purity uncertainty. Accrued interest over the loan tenure, which may run several months before a default is resolved through auction, adds a further claim on the collateral before proceeds can be applied to principal. Gold prices can also move materially in either direction during the recovery period. These factors together mean the real headroom is narrower than the headline LTV gap implies, which is why accurate fraud detection matters even within a buffered system.

How Gold Value Is Calculated

The RBI framework standardises valuation methodology across lenders. Gold value must be determined using:

- the lower of the previous day’s price or the 30-day average price, and

- prices published by the India Bullion and Jewellers Association or recognised exchanges.

All jewellery is converted into a 22-karat equivalent value before applying the price benchmark. For example, 18K jewellery weighing 20 grams contains roughly 15 grams of pure gold. That pure gold quantity is converted into an equivalent 22K weight and valued using the applicable price.

What Happens If a Loan Defaults

If a borrower fails to repay, the jewellery may be auctioned. These auctions typically clear at slightly below melt value, often around 92–97%, because buyers account for refining costs and uncertainty around purity. This is another reason why conservative LTV ratios are necessary.

A System Built for Speed and Practicality Gold loan branches operate at high transaction volumes. A trained appraiser can often complete the entire assaying and valuation process in few minutes (depending of loan amount) per customer. This speed is one reason gold lending scales so effectively compared with other forms of collateralised credit. The system ultimately rests on three interacting safeguards:

- Human assaying expertise

- Conservative LTV limits

- Standardised regulatory valuation rules

Together they allow a decentralised network of branches to safely lend against jewellery owned by millions of households.

Gold loan assaying is not laboratory science. It is a practical screening system designed to answer a simple question quickly: is this genuine gold jewellery of roughly the claimed purity, or is it something else?

#indiagold #GoldLoan #Fintech #PersonalFinance #DigitalLending #GoldLoanAtHome #SmartFinancing #FinancialInclusion #InstantCredit #HassleFree #WorkingCapital #SMEFinance #BusinessGrowth