Stridhan Was Always Hers. Now It's Working for Her.

At indigold, roughly one in three of our borrowers is a woman.

We didn't design a product specifically for women. We didn't run a targeted campaign. We built something that removed friction from credit — and women responded. That number isn't a marketing outcome. It turns out it reflects a broader market reality we didn't fully appreciate until recently.

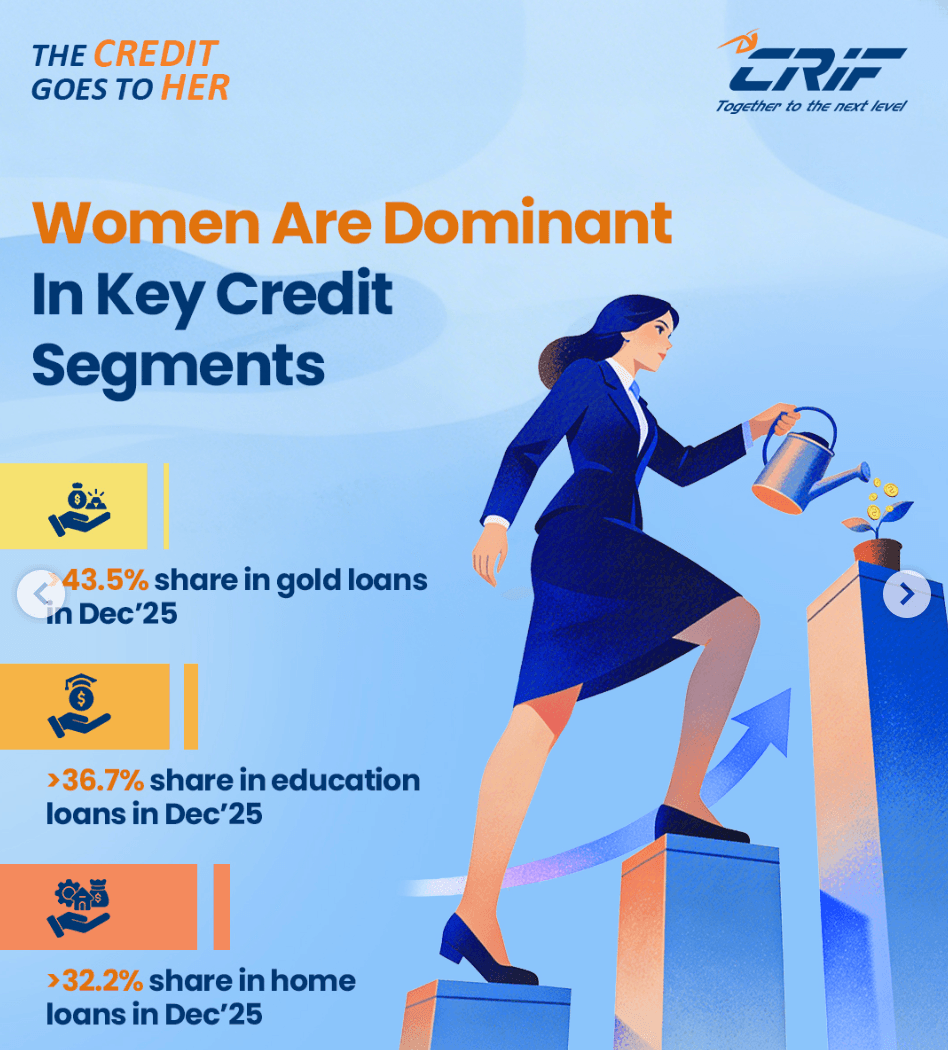

According to CRIF High Mark's The Credit Goes to Her report (March 2026), women hold a 43.5% share of gold loans across all lenders in India — the highest share of any credit product category in the country. Home loans: 32.2%. Education loans: 36.7%. Personal loans: 17.4%. Nothing comes close to gold loans. Women have effectively voted with their gold — and they've been doing it at scale.

India's Gold Is Largely Women's Gold

Indian households hold an estimated ~25,000 tonnes of gold, the largest private stockpile in the world. Women accumulate a disproportionate share of it — through marriage, festivals, inheritance, and personal savings. It is gifted, passed down, quietly held.

This isn't idle sentiment. It is the single largest financial asset that millions of Indian women own outright. And for most of history, it has simply sat there.

The Credit System Was Built for Someone Else

India's formal credit infrastructure was designed around one profile: a salaried individual with documented income, a bank account, and a CIBIL score. Miss any of these, and the door quietly closes.

Women — homemakers, agricultural workers, informal traders, self-employed entrepreneurs — have been disproportionately locked out. Not because they're poor credit risks. Because the underwriting criteria were built around a working profile that excluded them.

Think of it like a highway toll booth that only accepts one currency. If you don't carry that currency — a salary slip, a tax return, a credit history — you simply don't get on the road. The system doesn't ask what you own. It only asks what you earn.

The irony: the data shows women are actually better credit risks than men. CRIF High Mark's latest numbers put women's overall delinquency (PAR 31-180) at 2.8% vs. 3.3% for men. In gold loans specifically, the gap holds — 1.7% for women vs. 1.8% for men. The system has been excluding its more reliable borrowers.

Gold Shifts the Question

A gold loan doesn't ask how much do you earn. It asks what do you own. That is a fundamental rewrite of the underwriting logic — and it's precisely where women have an asymmetric advantage.

The practical benefits are real. A gold loan from a regulated NBFC typically comes at 12–20% per annum — meaningfully lower than a personal loan (18–24%), a credit card rollover (36–42%), or a moneylender operating in rural markets, whose rates can breach 48%. Disbursement happens in under an hour, with no committee approvals and no waiting periods.

And critically — the asset is preserved, not sold. A woman pledges her gold, uses the liquidity, and reclaims it when she repays. Unlike selling, which is a one-way door, a loan is a round trip. The gold comes back.

Stridhan: The Legal Standing Nobody Mentions

Gold received at marriage is legally a woman's personal property under Hindu succession law — and equivalent personal laws for other communities. It is not marital property. A husband has no legal claim over it.

This means a woman often has both the right and the means to pledge her gold independently — no spousal co-signing, no family approval required. That is genuine, legally grounded financial agency, sitting dormant in millions of households.

Doorstep Lending: The Part Nobody Talks About

There's one more dimension that changes the calculus entirely — where the loan happens.

Traveling to a branch with gold jewelry is a security risk in itself. You're visible, you're carrying something valuable, and in smaller towns, that walk is noticed. Beyond safety, there's the social dimension: in many communities, being seen entering a gold loan branch signals financial distress. For a woman managing household finances privately, that visibility is a genuine deterrent.

And then there's the practical reality. Many women — managing a household, caring for children or elderly parents — cannot simply leave when it suits them.

Doorstep lending dissolves all three problems at once. A loan officer comes home. The transaction happens inside four walls, at a time that works for her. The gold doesn't travel through a market. No neighbors observe. No explanations required. Safe, private, built around her life — not the other way around.

For many women, this isn't a convenience feature. It's the difference between accessing credit and not.

Gold Loans as a Gateway, Not Just a Product

Here's a data point that reframes the entire conversation. Among women who are New to Credit — getting their first-ever formal loan in India — gold loans are the #1 entry point by originations value, accounting for 23.7% of all new women borrowers entering the system (CRIF High Mark, Dec'25).

When a woman in India takes her first step into formal credit, the most likely vehicle is a gold loan. Not a personal loan. Not a microfinance product. Gold. That tells you something profound about where trust and accessibility actually meet for this borrower.

And this population is growing fast. Women borrowers grew at a 14.2% CAGR between Dec'20 and Dec'25 — compared to 8.2% for men. Their portfolio outstanding grew 23.4% YoY in Dec'25 vs. 16.7% for men. Active loans grew 14.8% YoY — more than double the rate for men. This is not a niche trend. It is a structural shift.

What They Actually Use It For

When you speak to women borrowers at the ground level, the use cases are rarely abstract. A school fee deadline. A hospitalization bill that arrived before the harvest. Inventory before a festival season. A bridge between when a payment is due and when the next income arrives.

Productive, time-sensitive credit needs. They don't need a 30-day processing cycle. They need liquidity today, with dignity — without justifying the purpose to a branch manager or explaining the situation to a family member. A gold loan provides exactly that.

The Gap We Haven't Fixed Yet

One in three of our borrowers being women is a start. It is not a finish.

India now has 8.9 crore active women borrowers in the formal system (Dec'25). Women hold 43.5% of all gold loans outstanding. Their credit quality is better than men's across nearly every product. And yet the demographic most structurally suited to a gold loan — the one with the asset, the need, the repayment discipline, and in many cases the legal right to pledge independently — has historically been the least targeted by the industry.

Awareness is low. Comfort with financial institutions has been built through years of exclusion. The industry has largely treated women as incidental borrowers rather than a primary customer.

That is starting to change. The data says it should accelerate.

Source: CRIF High Mark — "The Credit Goes to Her", March 2026