Why Bullet Schemes Face a Reckoning

The Reserve Bank’s new gold loan directions—the RBI (Lending Against Gold and Silver Collateral) Directions, 2025, notified on June 6, 2025 and effective April 1, 2026—are about to fundamentally reshape how gold loans work in India. While the headlines focus on LTV limits, the real disruption lies in a seemingly technical detail: for bullet repayment loans, LTV must be calculated on the total amount repayable at maturity—not just the principal.

Let me show you exactly what this means with real numbers.

The Problem: A Real Example Consider a typical large gold loan in today’s market:

- Gold pledged: ₹20,00,000 market value

- Loan amount: ₹14,50,000

- Booking LTV: 72.5%

- Interest rate: 24% per annum (note: this is at the higher end of market rates, which typically range from 10–26% depending on lender and product)

- Repayment: Bullet (full amount at 12 months)

- Loan category: Personal consumption >₹5 lakh

At first glance, a 72.5% booking LTV looks conservative and safe. But here’s the catch.

Under the new RBI framework:

- Total due at maturity: ₹17,98,000 (₹14.5L principal + ₹3.48L interest at 24% simple interest)

- LTV at maturity: ~90% (89.9%)

- RBI limit for consumption loans >₹5 lakh: 75%

- Breach: ~15 percentage points

A loan that looked perfectly compliant suddenly breaches regulatory limits by a massive margin once interest accrual is factored in.

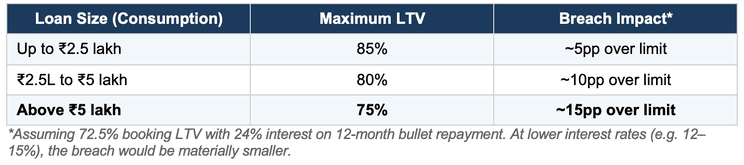

Understanding the Tiered LTV Framework The RBI has introduced a three-tier structure specifically for consumption loans, and the tier your loan falls into matters significantly. (Note: income-generating loans such as business or agricultural credit are governed separately and are not subject to this tiered structure.)

The tiered structure creates a challenging outcome: larger consumption loans face increasingly severe compliance constraints. The very segment that drives profitability for many lenders—high-value loans—faces the toughest limits.

Important regulatory context: If an LTV breach continues for more than 30 consecutive days, an additional standard asset provisioning of 1% applies. Normal provisioning can resume only after the LTV is restored and remains compliant for at least 30 consecutive days. Further, if the LTV remains in breach at maturity, the loan cannot be renewed or topped up until full repayment is made.

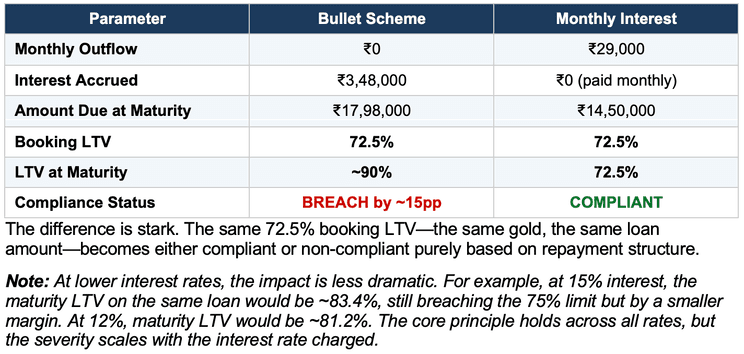

The Critical Comparison: Bullet vs. Monthly Interest Here’s how the same ₹14.5 lakh loan performs under different repayment structures:

What Lenders Must Do to Stay Compliant For lenders offering bullet schemes on large consumption loans, the math is unforgiving. Using our ₹14.5 lakh example, here are the options:

Option 1: Dramatically Reduce Booking LTV

To maintain bullet structure and stay compliant at 24% interest:

- Reduce booking LTV from 72.5% to ~60.5%

- Maximum loan: ~₹12.1 lakh (down from ₹14.5 lakh)

- Impact: ~16.6% reduction in loan size

This aligns with estimates from Vinod Kothari Consultants, who noted lenders may need to limit initial LTV to approximately 63–64% at industry-typical rates of 17–18%. At 24%, the constraint is even tighter.

Option 2: Transition to Monthly Interest Payment

Customers pay ₹29,000 monthly interest, principal due at end:

- Maintains full ticket size (₹14.5 lakh)

- LTV stays at 72.5% throughout tenure

- Requires collection infrastructure and customer education

- Monthly cash flow for lenders

Option 3: Hybrid Periodic Interest Servicing

Customers pay interest quarterly or semi-annually. This reduces accrual sufficiently to stay compliant while maintaining some bullet-loan flexibility. Strikes a middle ground between Options 1 and 2.

Industry Impact and Competitive Dynamics These changes will fundamentally reshape the gold lending landscape. Lenders who built their market position on high-LTV bullet schemes for large consumption loans—arguably the most profitable segment—face the steepest adjustment:

- Revenue Impact: A potential 16–17% reduction in average ticket size at higher interest rates translates directly to revenue pressure, unless offset by volume growth or a shift to periodic-interest products

- Operational Transformation: Moving to monthly or periodic interest collection requires significant technology and process changes

- Customer Behaviour: Many borrowers specifically seek bullet schemes for zero monthly outflow—this value proposition is significantly constrained

- Competitive Positioning: Lenders already offering non-bullet products have a structural advantage in the transition period

- Cooperative Banks and RRBs: These institutions face an additional constraint—bullet repayment loans are capped at ₹5 lakh per borrower, further limiting the segment

The winners in this transition will be lenders with robust digital infrastructure, diversified product portfolios, and strong customer engagement capabilities.

indiagold’s Position

At indiagold, our products have been designed around regular repayment schedules—periodic interest and EMI-based structures—rather than pure bullet repayment models. This means our core product offering is naturally aligned with the new framework and requires minimal adjustment.

We’ve always believed that sustainable gold lending means encouraging disciplined repayment behaviour and maintaining conservative risk parameters. The new RBI guidelines validate this philosophy and, importantly, create a more level playing field by requiring all lenders to adopt similarly prudent practices.

More broadly, we view these regulations as positive for the industry. Clear, well-enforced prudential norms protect both borrowers and lenders, creating a healthier ecosystem for sustainable growth.

Looking Ahead: Opportunity in Disruption

The April 2026 deadline provides adequate time for thoughtful adaptation. Rather than viewing these changes as purely restrictive, forward-thinking lenders can leverage this transition to:

- Build more robust risk management and compliance frameworks

- Invest in technology infrastructure for collection and monitoring

- Enhance customer education and transparency

- Differentiate through customer experience rather than aggressive LTVs

- Develop sustainable business models aligned with regulatory prudence

The gold loan market isn’t shrinking—it’s maturing. According to ICRA, the combined gold loan market (banks and NBFCs) is projected to hit ₹15 lakh crore by March 2026. Indian households hold approximately 25,000 tonnes of gold, but the organised lending sector currently taps into only about 5.6% of this potential. The demand for gold-backed credit remains robust. What’s changing is the expectation that lenders operate with greater transparency, stronger risk management, and genuine customer-centricity.

The lenders who navigate this transition successfully will be those who recognise it as an opportunity to strengthen their competitive position through operational excellence and sustainable value creation—not those who view it as a constraint to be minimally complied with.

#GoldLoans #RBI #FinancialServices #NBFC #Fintech #IndiaGold #RegulatoryCompliance #LendingInnovation #FinancialInclusion #BulletLoans