₹8.1 Lakh Crore Stuck in Delayed Payments

₹8.1 Lakh Crore Stuck in Delayed Payments: Why Gold Loans Are the Working Capital Solution MSMEs Need

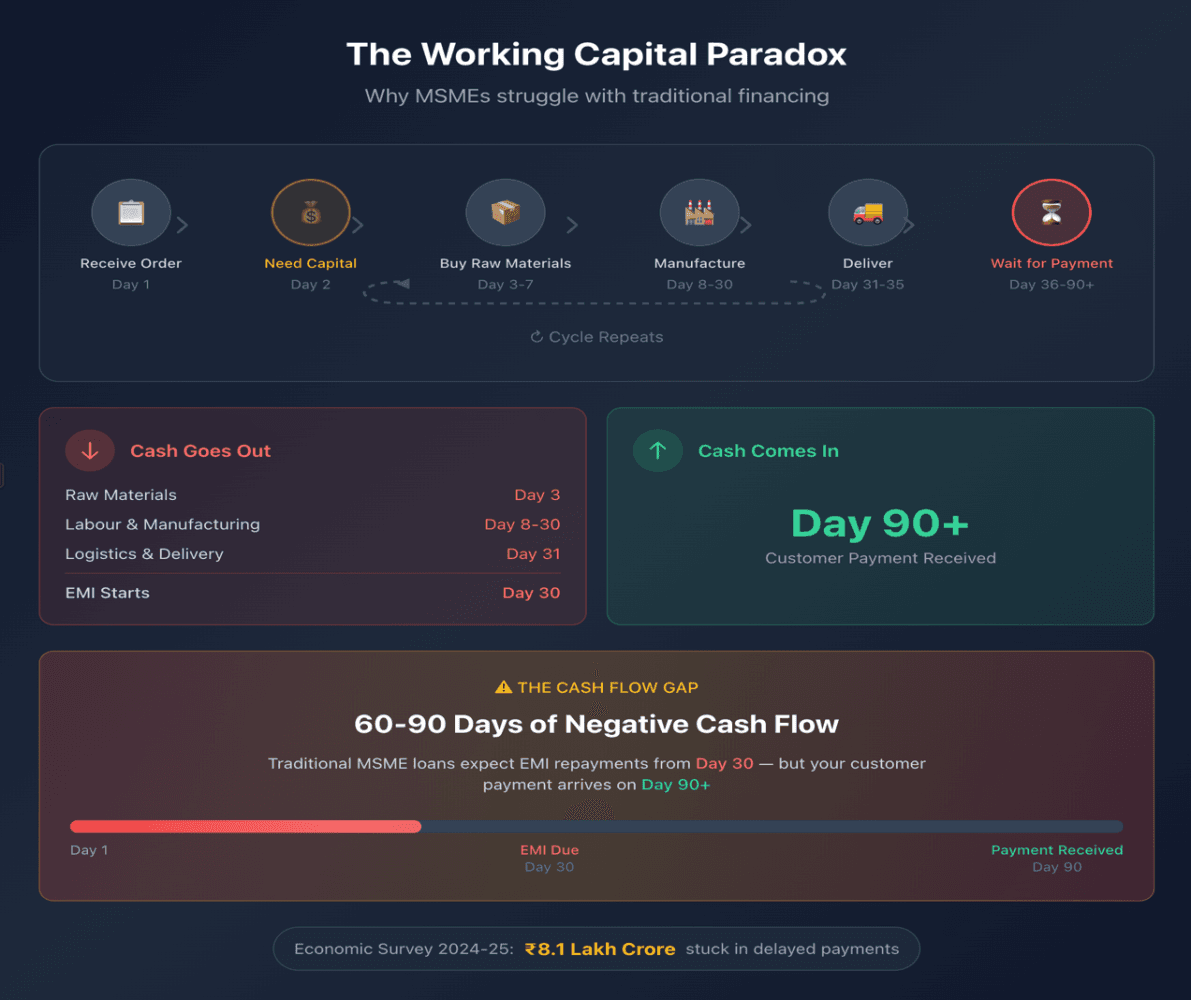

The Economic Survey 2024-25 has quantified what every MSME owner knows very well: ₹8.1 lakh crore is locked in delayed payments, impeding the working capital cycles of India's 7.47 crore micro, small and medium enterprises.

The law mandates payment within 45 days. The reality? 90-120 days is standard practice. And MSMEs can't push back — filing a delayed payment case risks losing the buyer relationship altogether.

Meanwhile, 27% of Indian MSMEs identify access to finance as their biggest obstacle. Limited collateral, weak documentation, lengthy approval cycles — the traditional lending system wasn't designed for businesses that need capital today to fulfil an order next week.

The Working Capital Paradox

Here's the typical MSME cycle: Receive an order → Need capital to buy raw materials → Manufacture and deliver → Wait 90-120 days for payment → Repeat

The challenge? You need money upfront, but your payment comes later. Traditional MSME loans expect you to start repaying EMIs from Day 30 — often 60-90 days before you've received payment from your customer.

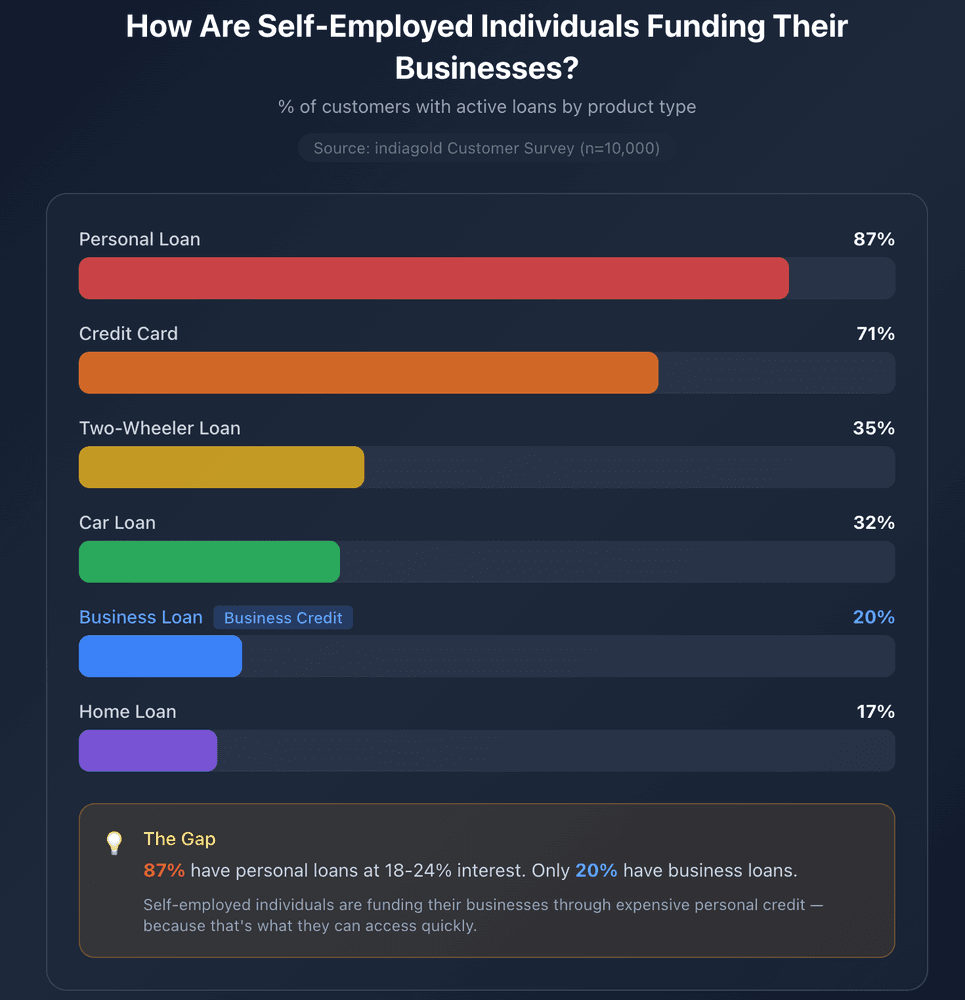

The Credit Gap is Real — And MSMEs Are Filling It Any Way They Can

At indiagold, we surveyed 10,000 customers to understand their existing credit behaviour. The findings were striking:

Self-employed individuals and MSME owners are funding their businesses through personal loans at 24%-48% interest rates (IRR is far higher) — because that's what they can access quickly. The business loan product, with its documentation requirements and week/s approval cycles, simply doesn't fit their cash flow realities.

Why Gold Loans Are Structurally Different

Indian households hold an estimated 25,000+ tonnes of gold. For self-employed individuals and MSME owners, this isn't just jewellery — it's an untapped working capital line.

- Speed of Disbursement Gold loans can be disbursed within hours. No income proof scrutiny, no business vintage requirements, no strict credit checks. The gold is the underwriting.

- Flexible Repayment Structures Unlike EMI-based loans, gold loans offer:

Interest-only payments: Pay just the interest monthly, settle principal at the end Bullet repayment: Pay everything at maturity Renewals: Extend the tenure if your receivables are delayed This structure aligns with MSME cash flows — you're not forced to repay principal before your customer has paid you.

- Appreciating Collateral Here's what makes gold unique: the collateral itself appreciates over time (up 150% in just 2 years).

Gold prices have risen consistently over the long term. This means the same jewellery that got you a ₹10 lakh loan today could qualify for ₹12-15 lakh next year — without any change in your business metrics, income documents, or credit score.

For an MSME, this is a growing credit line that expands with the asset, not with paperwork.

The Market is Already Moving

The CRIF High Mark "How India Lends" Report for Q2 FY26 shows a clear trend: gold loan adoption is rising among MSMEs and New-to-Credit (NTC) borrowers.

This isn't surprising. When traditional business credit requires collateral you don't have and documentation you can't produce, gold — which you already own — becomes the logical funding source. MSMEs are beginning to unlock the value of an asset that has been sitting idle in bank lockers and home safes

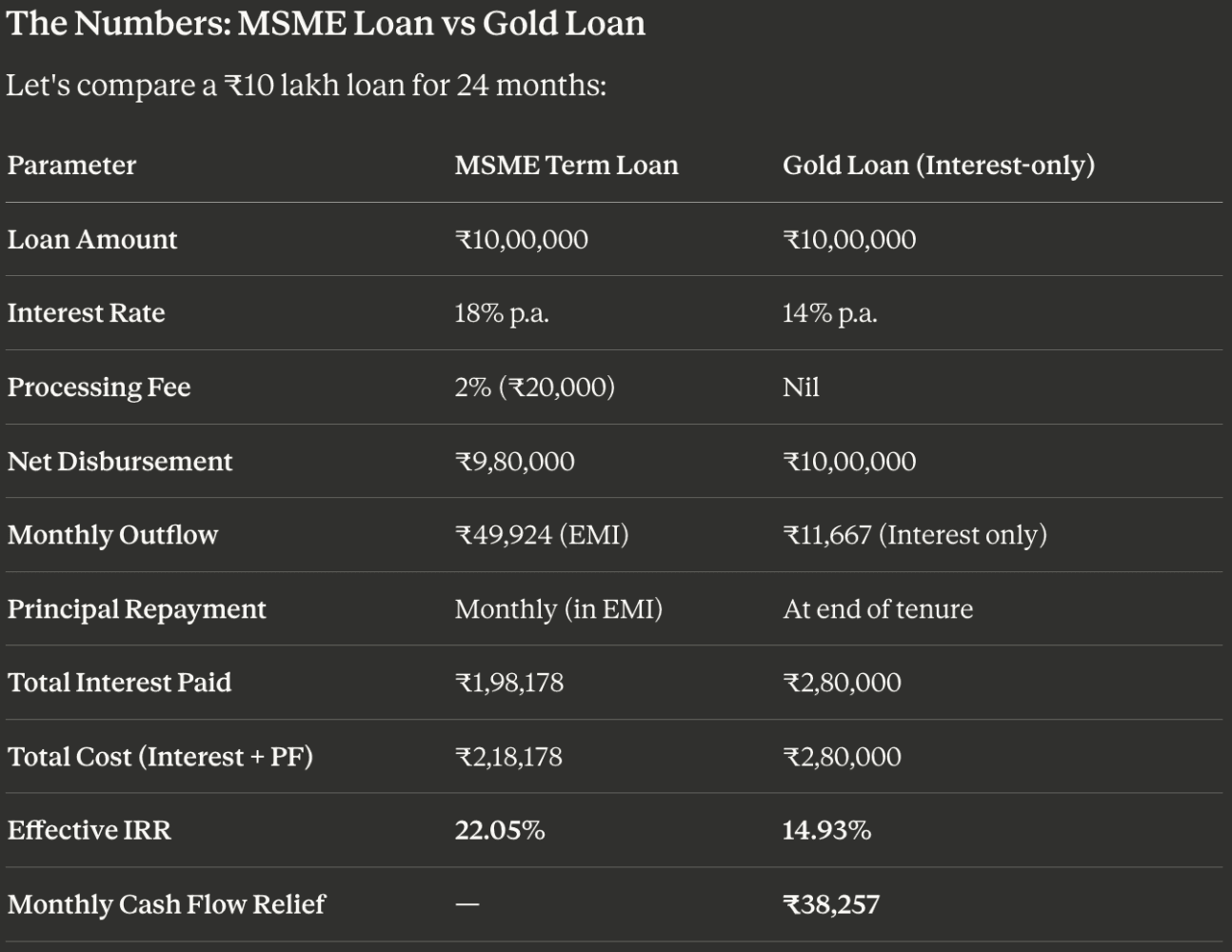

The Numbers: MSME Loan vs Gold Loan

Look beyond the total interest figure. The effective IRR tells the real story: 22.05% vs 14.93%.

Yes, you pay more absolute interest with the gold loan over 24 months. But:

You receive ₹20,000 more upfront (no processing fee) You retain ₹38,257 extra per month in your business Your true cost of capital is 7% lower For a business waiting on receivables, that monthly liquidity is worth far more than the interest differential. This ₹38,257/month difference is not savings — it is released working capital cash flow. That distinction matters.

What happens when a small business owner improves cash velocity instead of paying it to the bank?

Over 12 months, that becomes ₹4,59,084 of deployable capital. Typical trading/retail gross margins: 12–25% per cycle Inventory turns: 8–12 cycles/year.

Impact: They didn’t “save” ₹4.6L. They converted financing efficiency into ₹6–8L additional profit.

Small Indian businesses are usually inventory-constrained, not demand-constrained. That is how working capital arbitrage compounds.

The Structural Advantage

When the Economic Survey calls for "cash-flow-based lending," it's acknowledging that traditional collateral-based underwriting doesn't work for small businesses with irregular income patterns.

Gold loans are, in effect, asset-backed cash-flow lending:

Your gold provides the security The flexible repayment matches your actual cash flows You're not penalised for the timing mismatch between expenses and receivables Your credit line grows as gold prices appreciate What Needs to Change

The ₹8.1 lakh crore locked in delayed payments won't unlock overnight. But ensuring MSMEs have access to working capital that matches their cash flow realities? That's a solvable problem.

For gold loans to truly serve the MSME segment at scale, we need:

Higher LTV ratios — allowing businesses to unlock more value from their gold (will write about income generating gold loans soon) Seamless renewal processes — so working capital lines can be extended without friction Digital-first experiences — reducing the time from application to cash-in-hand The gold is already there. The demand is already there. It's time to build the bridge.

Sources:

Economic Survey 2024-25, Ministry of Finance CRIF High Mark "How India Lends" Report, Q2 FY26 indiagold Customer Survey (n=10,000) #MSME #WorkingCapital #GoldLoan #EconomicSurvey #FinancialInclusion #SmallBusiness #IndiaEconomy