300,000 branches needed to serve gold loan demand

The organised gold lending sector has grown rapidly — bank loans against gold jewellery went from ₹7.5 lakh crore (May 2024) to ₹10 lakh crore (May 2025) & now has crossed ₹16 lakh crore. This is impressive growth but...

The unorganised market — pawn shops, local moneylenders — has expanded roughly 5x since 2014 to an estimated ₹28 lakh crore.

Even in a well-served locality like Koramangala in Bengaluru (a 6.9 sq km IT hub), there are approximately 23 organised gold lenders versus 150 unorganised ones. Across Karnataka, the ratio is ~5,000 organised versus ~23,000 unorganised (source: Sulekha data scrub, Karnataka Department of Co-Operation).

The question worth examining: why does the unorganised market keep growing despite better rates, consumer protection, and institutional trust on the organised side?

The answer, in most cases, is proximity. Gold lending for retail borrowers is typically emergency credit — medical bills, seasonal business capital, school fees. For emergency credit, proximity outweighs price. When the nearest branch is 10-40 km away, borrowers go to whoever is closest. And in much of India, that's the local moneylender charging 36-100%+ per annum.

The Distribution Gap — By the Numbers

In rural India, one bank branch serves approximately 16,000 people. In urban India, it's about 4,400. To bring rural India to even the urban branch-per-capita ratio, you'd need approximately 1.5 lakh additional branches. To adequately serve gold loan demand specifically, industry estimates suggest ~3 lakh branches would be needed.

Some specific examples: in Shravasti (UP), about 15 villages share a single bank branch. In Nandurbar (Maharashtra), it's 17 villages per branch. 48% of India's population resides in villages with fewer than 4,000 people — a population count at which operating a full-service branch is not financially viable.

This is a structural distribution constraint, and branch expansion alone — while essential and ongoing — will take years to close the gap. The question is what can complement branches in the interim to extend the reach of regulated lending.

India Already Has Proven Doorstep Financial Service Models

Doorstep delivery of financial services is not a new concept in India. Two models in particular have demonstrated that regulated services can be delivered at customers' homes with appropriate process controls.

Business Correspondents (BCs): Out of 1.59 lakh Sub-Service Areas (SSAs) across the country, Business Correspondents now cover 1.26 lakh — compared to 0.33 lakh covered by bank branches. Near-universal banking access in over 99% of villages was achieved through the BC model. The precedent is clear: branch infrastructure alone could not have delivered this reach.

SBI's Doorstep Banking Service (DSB): State Bank of India and 11 other public sector banks deliver cash pickup and delivery at customers' homes through outsourced Doorstep Service Agents (DSAs), governed by a Board-approved policy (Version 5.0, dated 20.09.2024) and detailed operating instructions (Annexure V, PBBU-LIMA Department). The framework permits outsourced agents to handle cash — a fungible asset — at customer premises, using process-based safeguards: OTPs, verification codes, SMS confirmations, web portal tracking, Case IDs, and fidelity insurance. No proprietary technology is required. Cash pickup/delivery is capped at ₹20,000 per transaction. Services are available within 5 km of the home branch.

This is a regulatory approved framework in active operation. Outsourced agents handle physical cash at customers' doorsteps with process controls and clear liability assignment.

The proposed doorstep gold loan framework uses NBFC employees (not outsourced agents), handles a non-fungible, uniquely identifiable asset (not cash), and proposes stricter safeguards than what RBI has already approved for doorstep banking. By construction, it is a more conservative model than the already sanctioned model.

What Customers Report — Survey Data

A customer research survey (sample size: 2,017 borrowers who chose gold loan at home) found the following reasons for their preference:

- 60% cited greater convenience

- 58% cited safety — no need to carry gold outside

- 56% cited privacy — reduces stigma associated with visiting a gold loan branch

- 56% cited simpler process — managed through app/website

- 56% said they can involve family in the process

In a separate, larger survey (n = 3,513 customers), 57% preferred gold loan at home over gold loan at branch. Among those who chose the branch, the primary reason was proximity — they already lived close to a branch and had lower safety concerns about carrying gold.

The stigma dimension is worth understanding. In small-town and semi-urban India, visiting a gold loan branch is a visible, public act. For families where gold is tied to social standing, this visibility deters formal borrowing. One respondent — a 44-year-old salaried woman from Bengaluru — stated: "Did not want to carry gold outside home. Can't take gold to office as well. Don't know what others feel about taking a GL."

A particularly relevant data point: among new-to-gold-loan (NTGL) customers — people taking a formal gold loan for the first time — 38.5% came through the doorstep model during the period it was operational (October 2023 – March 2024). After the regulatory pause forced a branch-only model (October 2025 – March 2026), that NTGL percentage dropped to 31.5%. This suggests the doorstep model was bringing new borrowers into the organised lending system — borrowers who, without this option, may have continued with informal lenders.

(Source: Customer research surveys, n=2,017 and n=3,513; disbursement data from operational NBFC records.)

Addressing the Core Question: Is It Safe?

Gold is not cash. A lost ₹500 note can be replaced with another identical ₹500 note. A grandmother's wedding necklace cannot. Gold jewellery carries sentimental value that monetary compensation does not fully address. Any framework for doorstep gold loans must account for this emotional dimension — it must do more than ensure financial restitution; it must minimise the probability of loss to near-zero. This concern is legitimate and central to the discussion. Here is how the operational framework addresses it, stage by stage.

Personnel Standards

Every doorstep employee is a full-time NBFC employee — not an outsourced agent, not a gig worker. Background verification includes police verification, residential address verification, and employment history checks. Mandatory training and certification covers gold assaying, tamper-proof packaging, customer interaction protocols, and emergency response. Each employee is assigned to a specific branch, with a fixed roster maintained by the branch and communicated to customers before each visit.

For reference, the MHA's 2016 Draft SOP for cash transportation under the PSAR Act, 2005 requires police clearance, residence verification (3+ years at address), reference checks with 2 previous employers, and two guarantors for cash-in-transit personnel. Doorstep gold loan employee standards are comparable, applied to a significantly lower-value, lower-risk context (individual household transactions versus crores in currency).

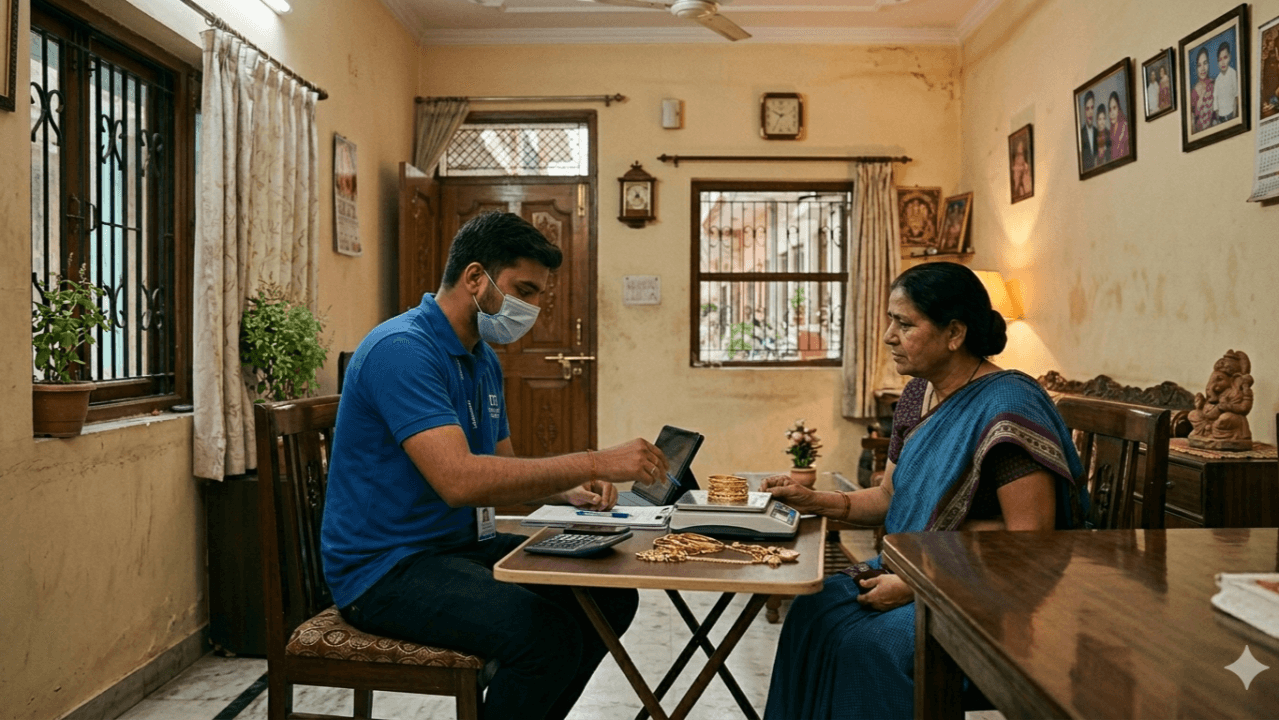

At the Customer's Doorstep

The service is customer-initiated — no cold calls, no unsolicited visits. The customer receives the designated employee's name, photograph, and unique ID via SMS/app before the visit.

At the doorstep, identity verification is two-way: the customer verifies the employee's credentials via a one-time verification code (OTP or service code) sent to their registered mobile. The employee simultaneously verifies the customer's identity. This mirrors the same two-way verification protocol used in SBI's DSB framework (Annexure V, Para 4.1–4.3).

Before any gold is handed over, the customer receives a Key Facts Statement in their vernacular language covering interest rate, total cost, repayment schedule, auction policy, and — critically — how the gold will be transported to the branch vault and what happens if something goes wrong during transit. The customer also provides explicit recorded consent for gold transit. And the customer must be offered the option to carry the gold to the branch themselves if they prefer.

Each ornament is individually photographed, weighed on a calibrated electronic scale, and assessed for purity. A certificate is issued in duplicate with purity, weight (net of stones), and photograph of each ornament. Disbursement goes directly to the borrower's verified bank account — 100% digital, no cash handling.

The Maker-Checker Architecture

This is a structural point worth understanding. In the doorstep model, the field employee assays the gold but cannot determine the final valuation or approve the loan amount. All assaying data — photographs, weights, purity readings — is transmitted to a centralised credit team. An independent credit officer reviews the data and sets the valuation. A separate function handles the disbursal decision.

In a traditional gold loan branch, the same appraiser often assays, values, and books the loan. Where maker-checker exists, the two individuals typically sit in the same branch, creating collusion risk. The doorstep model separates these functions structurally — the maker and checker operate in different environments with different information access. This segregation of duties is a core internal control principle that the doorstep model implements by design.

Gold in Transit — Why Gold Is Inherently Safer to Transport Than Cash

This is counterintuitive but factually important. Cash is completely fungible — a stolen ₹500 note is indistinguishable from any other ₹500 note. It's immediately usable and difficult to trace. Gold jewellery is the opposite: each ornament is unique (specific design, weight, purity, hallmark), it has been photographed and documented, and a stolen ornament must be melted or sold to a buyer who risks receiving stolen property. The forensic record — photographs, weight, purity signature — makes gold a high-risk, low-reward target for a rational thief.

The operational transit controls:

- Gold is sealed in tamper-evident bags (ISO 17712 or equivalent) with unique serial numbers, in the customer's presence. Any attempt to open or tamper visibly destroys the seal.

- GPS tracking is active on the employee's smartphone from the moment of sealing to vault ingestion. Route monitoring flags deviations (500m from prescribed route or 15 minutes beyond expected transit time).

- Maximum transit window is prescribed (e.g., 4 hours from sealing to vault). No intermediate stops, no overnight holding.

- Mandatory same-day vault ingestion — the gold must reach the branch vault the same day.

- Transit insurance at up to 120% of jewel value, effective from the moment of sealing. The NBFC bears full liability to the customer regardless of insurance status — the customer is made whole immediately.

At the branch vault, the tamper-evident seal is inspected under CCTV before opening. Gold is re-weighed and reconciled against the doorstep record. Weight tolerance: ±0.1g. Any discrepancy triggers an automatic incident protocol.

For context, India's Cash-in-Transit (CIT) industry — CMS Info Systems, SIS Prosegur — already transports ₹37,000+ crore daily using standardised processes: GPS tracking, tamper-evident packaging, designated personnel, and insurance. Even at full scale, doorstep gold transit would represent a fraction of this volume. Gold, being non-fungible and harder to liquidate than cash, is inherently safer to transport under the same principles.

Risk Containment: The Compartmentalisation Principle

Even with all safeguards, the framework must answer: what happens if something goes wrong? The design principle is compartmentalisation — ensuring that a single incident cannot cascade into systemic risk.

- Per-employee daily limits cap the maximum collateral value any one person handles.

- Per-transaction cap limits maximum exposure per transit.

- One-packet-per-employee-at-a-time: no pooling of multiple customers' gold in a single transit.

- Branch-level and entity-level exposure limits ensure the vast majority of collateral is always in branch vaults, not in transit.

In the worst-case scenario — a robbery — the maximum loss is bounded, insured, and the customer is made whole immediately by the NBFC. This is the same principle under which SBI's DSB framework operates: the bank bears full liability for the DSA's acts (Policy v5.0, Section 7.1).

The Track Record RBI-registered fintech NBFCs have operated doorstep gold loans for over 5 years. The combined operational footprint: 7.7 lakh+ loans originated, ₹23,000+ crore disbursed, ~1.9 lakh unique customers served, across 75+ cities, backed by ₹500+ crore in technology investment.

The safety record across these operations:

- In-transit gold theft or loss: virtually zero incidents

- Insurance claims related to gold loss: zero filed

- Net credit loss (including through COVID): zero

- Customer NPS: 78–80% (significantly above financial services industry average)

The Broader Opportunity

India's RBI Financial Inclusion Index has risen from 53.9 (March 2021) to 67.0 (March 2025) — a reflection of sustained, progressive regulatory effort. Branch expansion continues apace, with NBFCs collectively planning 3,000+ new branches.

Doorstep gold lending is not a substitute for this expansion. It is a complement — designed to extend the branch's reach to customer segments that branches alone may take time to serve: elderly borrowers with mobility constraints, the 26.8 million persons with disabilities (Census 2011), women in communities where travelling to a gold loan branch carries social barriers, and rural borrowers far from the nearest branch.

The gold is already in India's homes. The demand is already there. A process-led framework — with appropriate controls, graduated permissions, and regulatory oversight — can help connect the two through the regulated system rather than leaving it to the ₹28 lakh crore unorganised market.

The operational evidence across 7.7 lakh+ transactions and 5+ years of operations suggests the model can work safely. The question now is whether a measured, evidence-based regulatory pathway can be established.

Data sources: RBI bulletins, PwC India "Striking Gold" report (August 2024), CRIF High Mark reports, IBEF, World Gold Council, Census 2011, customer research surveys (n=2,017 and n=3,513), MHA Draft SOP under PSAR Act 2005, SBI Doorstep Banking Policy v5.0 and Annexure V operating instructions, Unified Fintech Forum representation to RBI (April 2026), and operational disclosures from leading doorstep gold loan NBFCs.