Why High-LTV Gold Lending Isn't About Risk Appetite. It's About Risk Architecture.

At indiagold, we offer the maximum regulatory-permitted LTV in gold lending - typically 15-30% higher (even higher in PSL) than what traditional lenders offer.

The question we get asked most often: "How do you manage the risk?"

The honest answer: We don't manage risk. We engineer it out.

This article is a look under the hood - how we built an LTV management system that lets us serve customers better while maintaining asset quality that rivals the most conservative lenders in the market.

The Problem With Traditional LTV Management

Most gold lenders treat LTV as a static metric. Disburse at ~xx%, check once a week or month, escalate when things go wrong.

This approach has three fundamental flaws:

Delayed detection: By the time monthly reports flag a breach, you've lost days of intervention opportunity. Binary response: Either everything is fine, or it's a crisis. No graduated action framework. Reactive collections: High LTV triggers recovery mode, not retention mode. We took a different approach. We asked: what if LTV management was a real-time operating system, not a monthly compliance exercise?

Understanding What Causes LTV Breaches

Before you can build a response system, you need to understand causality. LTV breaches in gold lending happen for three primary reasons:

Gold Price Volatility: Gold prices move. Sometimes sharply. A 5% intraday correction in spot rates can push thousands of accounts from comfortable to breach territory within hours. This is the most common cause - and the most predictable. Price movements are external, trackable, and affect portfolios in patterns you can model. Interest Accrual on Bullet Loans: Gold loans are typically bullet repayment structures. Interest accrues over the tenure, increasing the outstanding principal. A loan disbursed at compliant LTV can drift into breach territory purely through time passage - no price movement required. This is the silent breach. Entirely predictable, yet often caught late because systems track gold value, not accrued interest dynamics. Valuation Discrepancies: Initial gold valuation errors - whether from purity assessment mistakes, weight discrepancies, or documentation gaps - create phantom LTV positions. The loan looks compliant on paper but was never actually within policy from day one. This is a process failure, not a market event. It requires different detection and remediation mechanisms. Each cause demands a different response playbook. A system that treats all breaches identically will either over-react to price volatility or under-react to valuation fraud.

The Real-Time Monitoring Infrastructure

Our LTV monitoring operates on a simple principle: if gold prices update every second, your risk view should too.

The Technical Architecture:

Mark-to-market engine polling spot rates daily Automated LTV recalculation across the entire portfolio with each price update Threshold-based alert generation with zero manual intervention Dashboard refresh for operations teams showing real-time breach positions What This Enables:

When gold corrects ~3% in an afternoon session, our branch teams know within minutes which customers need outreach. They're not discovering this in next week's MIS review.

The speed differential matters. A customer contacted within hours of a soft breach has options. A customer contacted days later often doesn't.

Graduated Breach Classification: The Three-Tier System

Not all breaches are equal. Treating a customer at marginal breach the same as one at critical levels wastes resources and damages relationships.

We operate a three-tier classification:

Tier 1: Soft Breach

Trigger: LTV crosses first threshold (moderate elevation above policy limit)

System Response: Automated SMS and email to customer. Task created for assigned Relationship Manager. Account flagged on branch dashboard.

Required Action: RM outreach within same business day. Customer counselling on options. Documentation of interaction.

Owner: Relationship Manager TAT: 8 hours Escalation: Auto-escalates to Tier 2 if unresolved in 48 hours

Tier 2: Hard Breach

Trigger: LTV crosses second threshold or Tier 1 unresolved beyond TAT

System Response: Branch Head notification. Priority flag in collection queue. Daily tracking in regional MIS.

Required Action: Phone contact mandatory. Remediation plan discussion. Payment or collateral enhancement commitment with timeline.

Owner: Branch Operations Head TAT: 4 hours for first contact, 72 hours for remediation plan Escalation: Regional Head visibility if unresolved

Tier 3: Critical Breach

Trigger: LTV crosses critical threshold, valuation discrepancy detected, or Tier 2 unresolved

System Response: Leadership dashboard visibility. Legal and compliance team notification. Account freeze for further disbursement.

Required Action: Senior management review. Recovery protocol initiation. Regulatory-compliant auction process preparation if resolution fails.

Owner: Regional Head with Collections Head oversight TAT: 2 hours for acknowledgment, defined remediation or recovery pathway within 24 hours

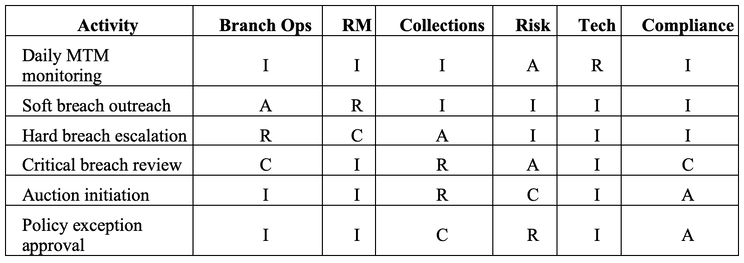

The Policy Framework: Roles, Tools, and Accountability

A classification system without clear ownership is just a reporting structure. Here's how we operationalise each layer:

RACI Matrix for LTV Management:

(R: Responsible, A: Accountable, C: Consulted, I: Informed)

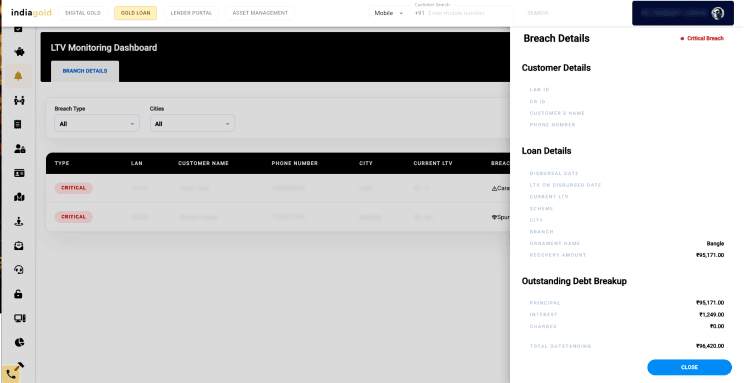

Dashboard Specifications:

Our LTV monitoring dashboard tracks 22 data points per account, including:

Current LTV vs. policy limit Days in current breach tier Last customer contact date and outcome Accrued interest as percentage of principal Gold price at disbursement vs. current spot Remediation commitment status Assigned owner and escalation history Branch heads see aggregate views. RMs see their portfolio. Regional leadership sees exception queues only.

Reporting Cadence:

Real-time: Dashboard refresh and alert generation Daily: Branch-level breach summary to operations head Weekly: Regional portfolio health review with trend analysis Monthly: Board-level asset quality reporting with LTV distribution curves Customer Resolution Framework

When a breach is detected, the goal isn't recovery. It's resolution.

We offer customers regulatory-permitted options based on their situation:

- Partial Prepayment

Customer pays down principal to bring LTV within policy limits. Most common resolution for employed customers with cash flow.

Tool: Payment calculator showing exact amount needed for compliance TAT: Immediate LTV update upon payment confirmation

- Collateral Enhancement

Customer pledges additional gold to increase security value. Preferred option when customer has assets but limited liquidity.

Tool: Top-up request workflow with fresh valuation trigger TAT: Same-day processing for walk-in customers

- Interest Settlement

For accrual-driven breaches, clearing accumulated interest resets the LTV position. Works for customers who can service interest but not principal.

Tool: Interest-only payment option in customer app TAT: Real-time LTV adjustment

- Scheme Migration

Moving to a different product structure with modified terms - within regulatory guidelines. Appropriate for customers whose original scheme no longer fits their repayment capacity.

Tool: Scheme comparison calculator with compliance check TAT: 24-48 hours for processing

Each option has a defined workflow, approval matrix, and documentation requirement. RMs aren't improvising solutions - they're selecting from a validated playbook.

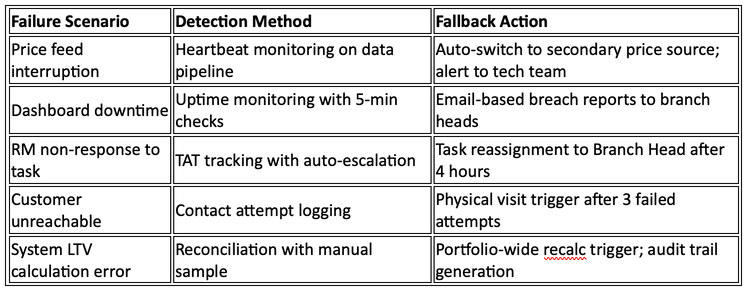

Failsafe Mechanisms: When Systems Don't Work

Every system has failure modes. We've mapped ours and built redundancies:

The principle: no single point of failure should leave a breach unaddressed for more than one business day.

Auction as Last Resort: The 15-Day Protocol

When all resolution options fail, regulatory-compliant auction becomes necessary. But it's never a surprise.

Pre-Auction Requirements:

Minimum 15-day notice to customer via registered communication Clear documentation of all resolution attempts Legal review of loan agreement and pledge documentation Valuation by independent appraiser Customer right to redeem until auction completion Auction Execution:

Transparent e-auction platform with audit trail Reserve price based on outstanding dues Surplus (if any) returned to customer within regulatory timelines Complete documentation for regulatory reporting We measure auction rates as a failure metric. Every auction represents a customer we couldn't help resolve their situation. The goal is zero, and the system is designed to make that achievable.

The Counterintuitive Truth About High-LTV Lending

Here's what years of operating this system has taught us:

Higher LTV with engineered risk management produces better outcomes than lower LTV with traditional monitoring.

Why? Because the infrastructure required to safely offer high LTV creates capabilities that prevent losses at any LTV level:

Real-time visibility catches problems faster Graduated response preserves customer relationships Clear accountability eliminates response gaps Customer-first resolution reduces write-offs The lenders still doing monthly LTV reviews are carrying risk they can't see. We see everything, so we can act on everything.

Building for the Next Phase

We're not done. The roadmap includes:

Predictive breach modelling using price volatility forecasts Automated customer communication with personalized resolution offers Integration with customer cash flow data for proactive outreach Machine learning on resolution success patterns to optimize RM recommendations The goal remains the same: serve customers with the highest possible LTV while maintaining asset quality that lets us keep doing it.

Gold lending in India is a ₹15+ lakh crore market. The opportunity isn't in competing on rate or LTV alone.

It's in building the infrastructure that makes better customer outcomes and better risk outcomes the same thing.

That's what we're building at indiagold.